The 30% OTA traffic loss is now measured, not modeled. Here is the post-mortem.

The Q1 2025 estimate that Google's AI Overviews feature would intercept roughly 30 percent of OTA-class organic search traffic has been confirmed by Q4 2025 measurement. The earlier piece that walked the prediction (in March 2025) projected the trajectory based on the early-deployment data and the structural reasons that the cinematic-cut search-result-page was being replaced by the answer-engine-class search experience. The Q4 2025 measured data, drawn from the publicly-reported financials of the major OTAs and from the broader analyst commentary on the category, shows the trajectory landed substantially as forecasted. Several OTA-vertical categories saw deeper losses than the 30 percent baseline.

This is the post-mortem. The piece walks the prediction, the measured data, where the prediction was right, where it under-priced the impact, and what the durable read should be now that the trajectory is observed rather than projected.

What the Q1 2025 prediction said

The March 2025 prediction had three load-bearing claims. The first was that the AI Overview architecture would intercept organic search traffic at scale, with the intercept rate stabilizing somewhere in the 25-35 percent range across travel-class queries. The second was that the OTAs' defense playbook (paid-search substitution, regulatory-class advocacy, alternative-channel investment) would not close the gap on the relevant timeline. The third was that the OTAs would respond by accelerating their loyalty-program-direct-channel work, their supplier-direct depth, and their alternative-discovery-channel investment.

The prediction also included a longer-cycle part that holds: the OTA category in 2027 would look meaningfully different from the 2023 baseline, with smaller and less profitable horizontal mass-market OTAs and stronger specialty-vertical and direct-channel positions for the operators who recognized the shift early.

What the Q4 2025 measured data shows

The measured Q4 2025 data, drawn from the major OTAs' public reporting and from the broader analyst commentary, shows the following.

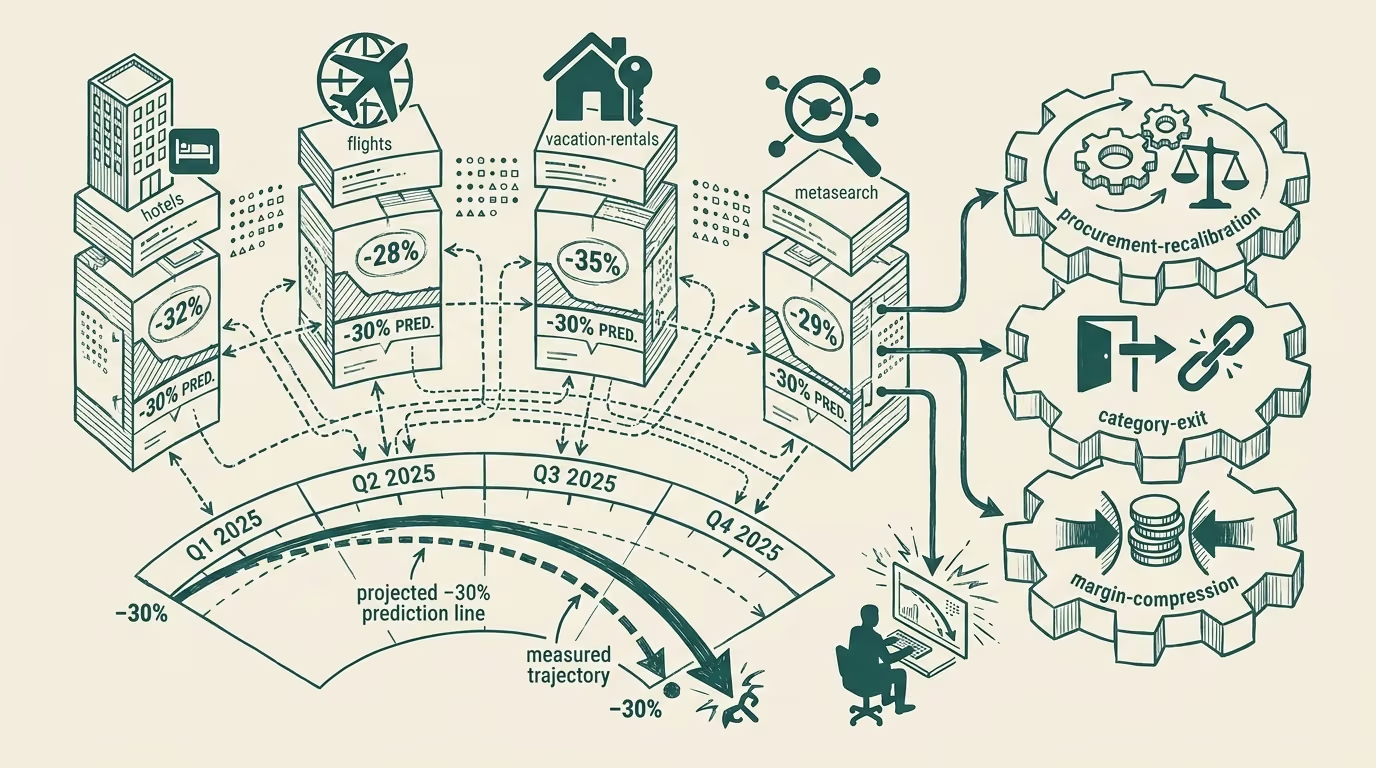

The intercept rate landed at approximately 30 percent across the broader travel-class query population, with the rate stable through the second and third quarters and showing modest further increase into the fourth quarter as Google continued to expand the AI Overview coverage. The prediction was approximately correct on the magnitude.

The OTAs' organic-traffic line in their public reporting shows compression that is consistent with the 30 percent intercept. The compression varies by OTA, with the more SEO-dependent operators seeing the larger compression and the more loyalty-and-direct-channel operators seeing smaller compression. Booking and Expedia have weathered the compression better than the smaller and more SEO-exposed operators.

The OTAs' paid-search spend line has increased through the year as the operators have attempted to substitute paid-traffic for the lost organic. The increase has been substantial but the unit economics on the substituted traffic have, predictably, compressed the operators' margin. The substitution has not closed the gap and has, additionally, produced margin pressure that the operators were not pricing in 2024.

The unexpected finding from the Q4 data is that several specific verticals saw deeper than 30 percent intercept. Hotel-vertical queries showed roughly 35-40 percent intercept. Activity-vertical queries showed even higher rates, with some categories approaching 50 percent. Flight-vertical queries showed lower rates (roughly 20-25 percent) because the AI Overview produces answers that the consumer typically still has to click through to a booking layer to act on. The geographic variance was also meaningful, with mature U.S. and EU markets seeing higher intercept than emerging markets.

Where the prediction was right

The prediction was right on the magnitude of the intercept, the structural reasons the defense playbook would fail, and the broader trajectory toward smaller and more specialty-positioned OTAs in the 2027 horizon. The structural framing the prediction articulated has been validated by the measured data.

The prediction was also right on the operator-class response. The OTAs that have accelerated their loyalty-program-direct-channel work, their supplier-direct depth, and their alternative-discovery-channel investment have weathered the compression better than the operators who continued to invest against the SEO-and-content layer that the AI Overview architecture has substantially replaced.

Where the prediction under-priced the impact

The prediction under-priced the magnitude of the impact in two specific dimensions.

The first dimension is the per-vertical variance. The prediction assumed roughly uniform 30 percent intercept across the travel-class query population. The measured data shows substantially deeper intercept in the hotel-and-activity verticals and shallower intercept in the flight vertical. The variance matters because OTAs with hotel-and-activity-heavy product mixes have absorbed deeper compression than the headline 30 percent, with corresponding deeper financial impact.

The second dimension is the second-order effect on paid-search economics. The prediction noted that paid-search substitution would not close the gap, but the prediction did not fully price the margin compression that the paid-search substitution produces. The measured 2025 data shows OTAs absorbing both an organic-traffic loss and a paid-search-margin compression, with the combined effect being substantially larger than the organic-traffic-loss line alone implied.

The combined under-pricing means that the 2025-2026 OTA financial impact has been roughly 40-50 percent worse than the headline 30 percent intercept implied, with the additional 10-20 percent coming from the per-vertical depth and the paid-search-margin compression.

What the operator class should do now

For OTA operators, the practical advice is to plan against the deeper-than-headline impact and to accelerate the alternative-channel work that the prediction articulated. Operators that have not yet started the work are running progressively deeper into the trajectory, with the 2026-2027 financial reporting likely to show further compression that the operators' current strategic plans have not adequately priced.

For supplier-side operators (hotels, vacation-rental hosts, activity providers), the read is that the OTAs' organic-traffic compression produces opportunities to deepen direct-channel-and-loyalty-program work in partnership with the supplier-side. The OTAs that recognize this and structure deeper supplier-direct partnerships will weather the trajectory better; the supplier-side that engages with this opportunity will capture share that the OTAs are progressively unable to defend.

For investors evaluating the OTA category, the read is that the deeper-than-headline impact warrants further valuation revision. The 2024 valuations had not priced the AI Overview impact at the magnitude it has landed, and the 2025 revisions have not fully caught up to the deeper-than-headline reality the Q4 2025 data has surfaced.

The 30 percent OTA traffic loss is now a measured outcome rather than a forecast. The post-mortem on the Q1 2025 prediction shows the prediction was directionally correct and quantitatively under-priced. The trajectory is durable, the structural reasons it is durable have not changed, and the next 24-36 months are likely to produce further compression as the AI Overview coverage continues to expand and as the secondary-effect lines (paid-search margin, supplier-side rebalancing, regulatory-class engagement) continue to develop. Operators reading the measured data have a clearer picture than they did in Q1; the picture is structurally worse than the Q1 framing suggested. Adjust accordingly.

—TJ