AI Overviews don't kill clicks. They kill the attribution chain that monetized the click.

Altexsoft's December 2025 analysis of travel-vertical referral traffic showed Google AI Overviews driving a measurable drop in clicks to OTA-class destinations. The drop confirmed the zero-click trajectory the SEO-class had been forecasting since AI Overviews launched in mid-2024. The trade press read it as another data point in the AI-replaces-search arc.

What's actually killed is sharper than the click. _AI Overviews don't kill clicks. They kill the attribution chain that monetized the click._

The two readings are not the same. The click-killed reading says: fewer users click through to the OTA, so OTA traffic drops. That's a volume claim. The attribution-killed reading says: even when the click happens, the chain that connects the click back to the original search intent is broken, so the ad-spend optimization that made the click profitable no longer runs. That's a unit-economics claim, and it bites whether or not the click volume drops.

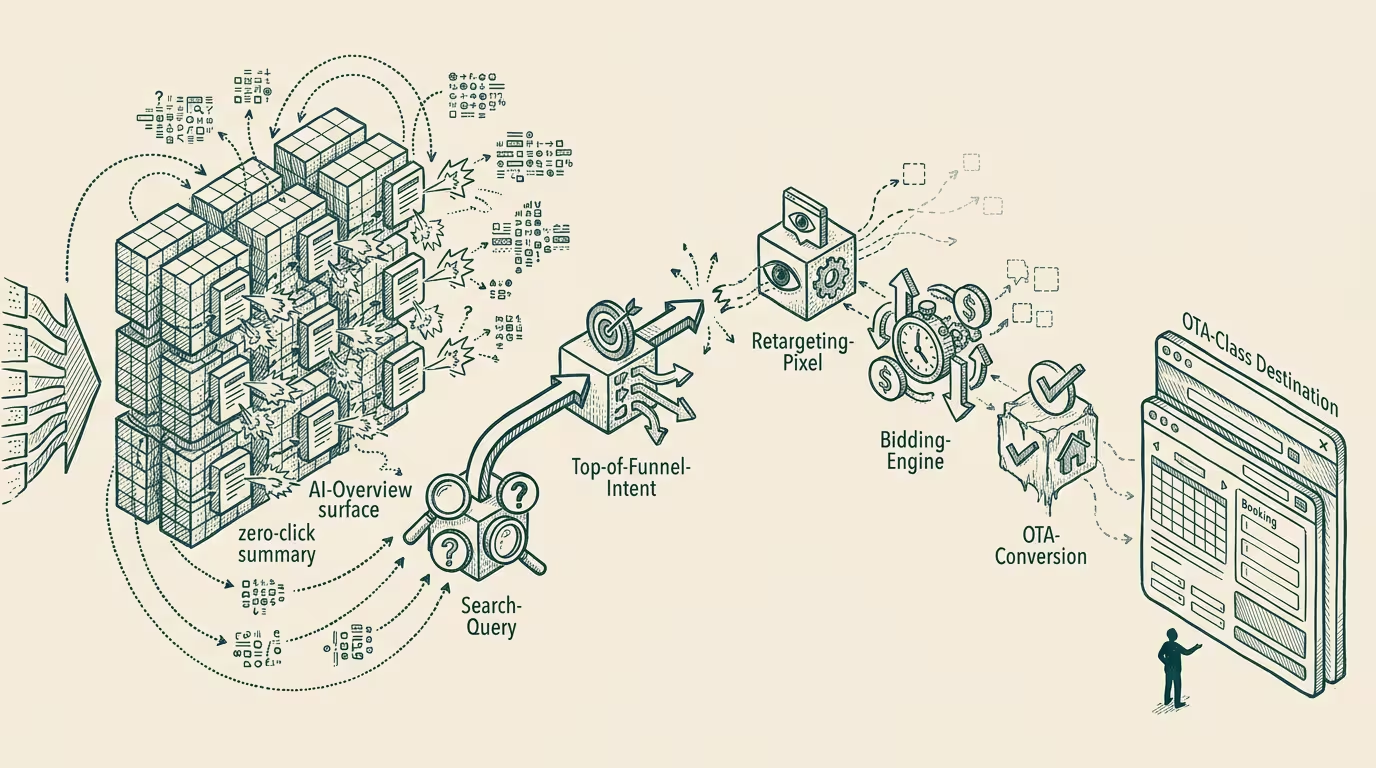

The pre-AI-Overviews mechanism was clean. A user searched "best Paris hotel", clicked through a Google ad to Booking.com, the ad-click tracking captured the conversion attribution, the ad-spend optimization model received the signal, the next-cycle bidding adjusted accordingly. Each click fed the bidding model, and the bidding model produced more efficient clicks. The flywheel ran on attribution.

The post-AI-Overviews mechanism breaks the flywheel even when the click survives. A user reads the AI Overview, the AI recommends specific hotels, the user clicks through to a hotel booking page (potentially the OTA, potentially the hotel direct, potentially a different OTA). The attribution data does not flow back through the search-intent layer because the click happened from an AI summary not from a tracked search-result link. The CAC math breaks before the OTA gets to model it.

The CAC reset that follows is structural, not cyclical. Travel-vertical paid-search budgets in 2024 were calibrated to a click-attribution model that no longer reflects the user's actual journey. Operators continuing to optimize bid strategies against the legacy attribution data are optimizing against a phantom. The model produces lower-quality predictions because the input data is missing the AI-Overview-mediated intent layer. CAC will rise as bid models miscalibrate, and the rise is structurally durable until either Google provides AI-Overview-attribution data (unlikely in the 2025-2027 window — Google has competitive incentive to obscure AI-mediated traffic from advertisers) or operators build alternative attribution mechanisms (post-click survey questions, customer-stated-source attribution, multi-touch modeling that weights AI-mediated touches).

What survives the reset is the operator-class mechanism that doesn't depend on the search-engine attribution chain. Loyalty-program data (the user identifies as a member at booking time, the lifetime-value-of-the-relationship is the attribution model rather than per-click ROI), branded-app installed-base (the user arrives via direct app launch, not via search, and the attribution is the install-event), partnership-class integration (credit-card co-brands, hotel-brand partnerships) where the attribution is contractual rather than click-based. Each is operator-level work that doesn't depend on the AI-Overview attribution layer. Operators with depth in these mechanisms are operating-coherent against the attribution-chain breakage. Operators dependent on click-attribution alone are absorbing CAC compression they cannot model.

The same shape recurs in healthtech and other categories on a 12-24 month lag. Healthtech symptom search (the user searches "what causes morning headaches", AI Overview answers, no click to a healthtech provider's lead-generation form). Healthtech provider lookup (the user searches "best primary care in Boston", AI Overview lists providers, no click to a referral platform). Each is the same attribution-chain breakage in a different vertical. Healthtech's CAC reset will surface in 2026-2027 with the same structural shape. Other categories — financial-services lead generation, insurance-quote shopping, automotive-research — follow on similar lags as Google AI Overviews expands category coverage.

Any operator business whose CAC math depends on click-attribution from search-engine traffic is operationally exposed to the AI-Overview attribution-chain breakage. The exposure is structurally durable through the next 24-36 months at minimum, possibly longer. Operators in exposed categories should be building proprietary-attribution mechanisms now and reweighting capital allocation away from paid-search budgets toward direct-relationship infrastructure.

What survives all of this is that the click-attribution model that powered 2010-2024 digital marketing is structurally degrading in the AI-Overview era, the attribution-chain breakage is a more important diagnostic than the click-volume drop, and the operator-grade strategy is to build attribution mechanisms that don't route through the search-engine layer. Operators who build the alternative attribution capture marketing efficiency that competitors lose. Operators who don't are watching CAC rise without being able to diagnose the cause from inside their existing measurement infrastructure.

AI Overviews don't kill clicks. They kill the attribution chain that monetized the click. The click that survives the AI summary is operationally valuable; the operator who captures that click also has to build new measurement to know it happened. The attribution work is the operator differentiation through 2026-2028. The categories that recognize the differentiation early capture the operator-level advantage; the categories that don't absorb the structural CAC compression as a market-wide cost.

—TJ