AI travel-planning crossed 50%. The OTA is the checkout now.

Marriott-commissioned research published in mid-2025 reported AI travel-planning usage rising from 26% in 2023, to 41% in 2024, to 50% in 2025. The trade-press read was "AI is reshaping travel planning." The durable read is that consumer behavior crossed the majority threshold in two years, AI is now the primary travel-planning surface, the OTA is the secondary checkout surface, and the OTA strategy that does not price the inversion is already losing share at the cohort margin.

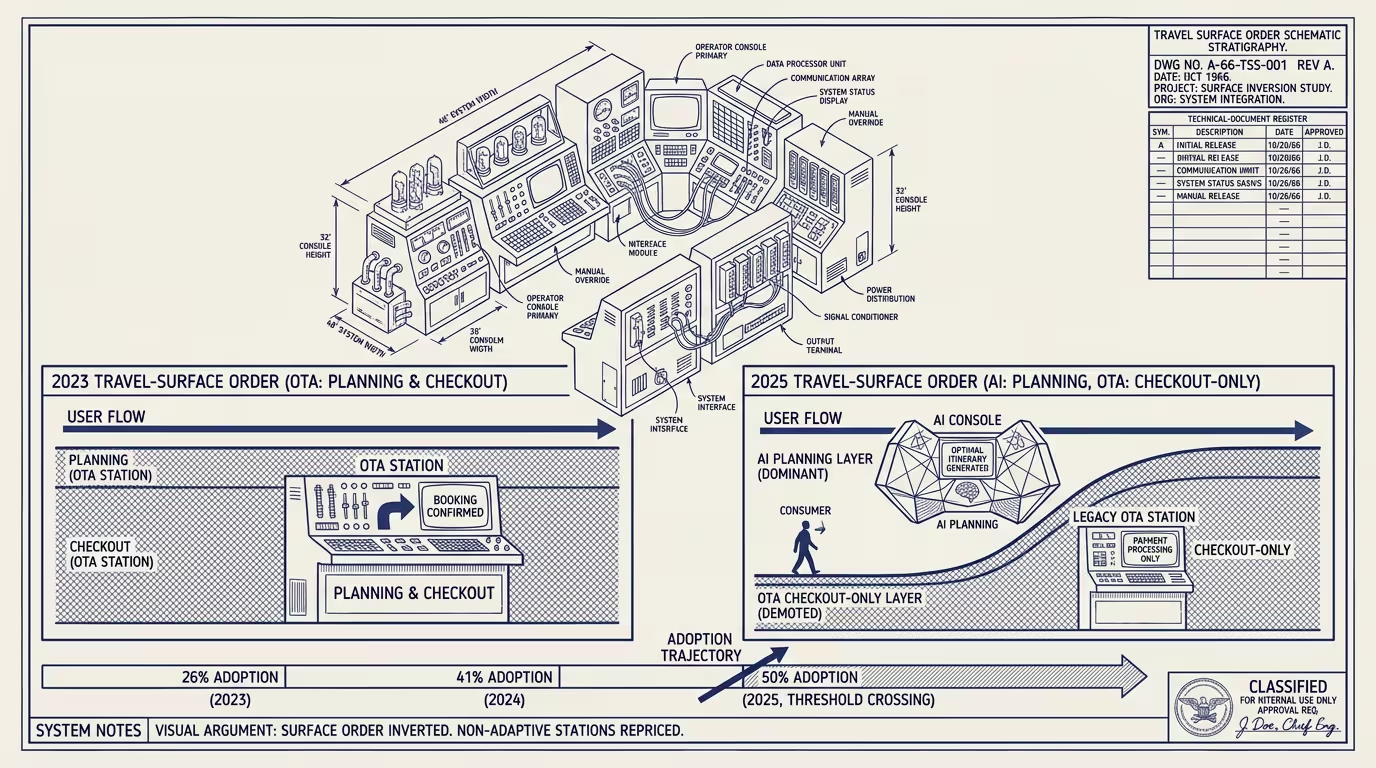

What changed structurally? The surface order. _Pre-2023, the OTA was the planning surface and the checkout surface — the consumer arrived at the OTA, browsed, and booked._ Post-2025, the AI is the planning surface and the OTA is the checkout surface — the consumer plans on the AI, then arrives at the OTA only to complete the transaction. The two surfaces are operationally distinct. The strategy that worked when the OTA owned both surfaces does not work when the OTA owns only the second one.

What's the OTA's traditional revenue mechanism? Discovery-margin: the consumer arrived without a specific intent, the OTA's recommendation engine surfaced options, the consumer booked one of the surfaced options, the OTA captured a margin on the booking. The mechanism required the OTA to own the discovery layer. In a 50%+ AI-planning world, the discovery layer is owned by the AI, and the OTA is bypassed during the discovery step. The consumer arrives at the OTA with a specific intent already formed.

What does that change for the OTA's checkout surface? Optimization target. The pre-inversion checkout was optimized for completion-friction reduction. The post-inversion checkout has to be optimized for AI-handoff reduction — the AI has done the planning, the consumer arrives with the intent, and the checkout has to convert the AI-formed intent without breaking it.

What's losing share in 2025? The OTA strategy that doesn't price the inversion. Booking, Expedia, and the long tail of regional OTAs are running 2024-shape strategies (calibrated to discovery-surface ownership) into a 2025-shape consumer behavior (AI-planning then OTA-checkout). The cohort that crossed to AI-first planning is, on the legacy OTA strategy, converting at lower rates than the OTA's mix-shifted historical baseline. The cohort-level conversion drag is the leading indicator of share loss. By 2026 the share loss is visible in the OTA's quarterly metrics. By 2027 the consensus read on the OTA category is repriced.

What survival paths exist? Two. Path one is preferred-checkout: the OTA wins the AI's checkout-handoff by being the most reliable, lowest-friction completion surface. Path two is recommendation-source: the OTA becomes the data-and-inventory provider that the AI references, capturing rents at the discovery layer through API-class integration rather than at the consumer-facing layer. Booking has elements of both strategies. Expedia has elements of neither. The strategy choice is the operator-class question for every OTA in 2025-2026.

Where does the cross-category pattern surface? Adjacent regulated-checkout categories. The same AI-planning-then-checkout-surface inversion is happening in healthcare-AI (consumer plans clinical research on AI, then completes the appointment booking on the platform), finance-AI (consumer plans portfolio decisions on AI, then completes the transaction on the broker), education-AI (consumer plans course selection on AI, then completes enrollment on the platform). Each category has its own inversion-velocity. Travel is one of the faster ones because the planning workload is well-suited to AI assistance and the checkout friction was already minimized. The cross-category implication is that any operator in any category whose value capture depends on owning the discovery layer has to expect the inversion within an 18-36 month window.

What survives all of this is that the 50% threshold is one of the cleanest visible markers of the AI-vs-OTA surface inversion in travel, the OTA strategy that does not price the inversion is operating-incoherent, and the operator-level question for every OTA in 2025-2026 is whether the company is positioned for preferred-checkout or for recommendation-source. The default — running the legacy strategy — is the position the OTAs that lose the most share by 2027 are running.

AI travel-planning crossed 50%. The OTA is the checkout now. The OTAs that recognize the inversion and reposition are the OTAs whose 2027 strategic position is durable. The ones that don't are running a discovery-surface strategy in a category where the discovery surface no longer belongs to them.

—TJ