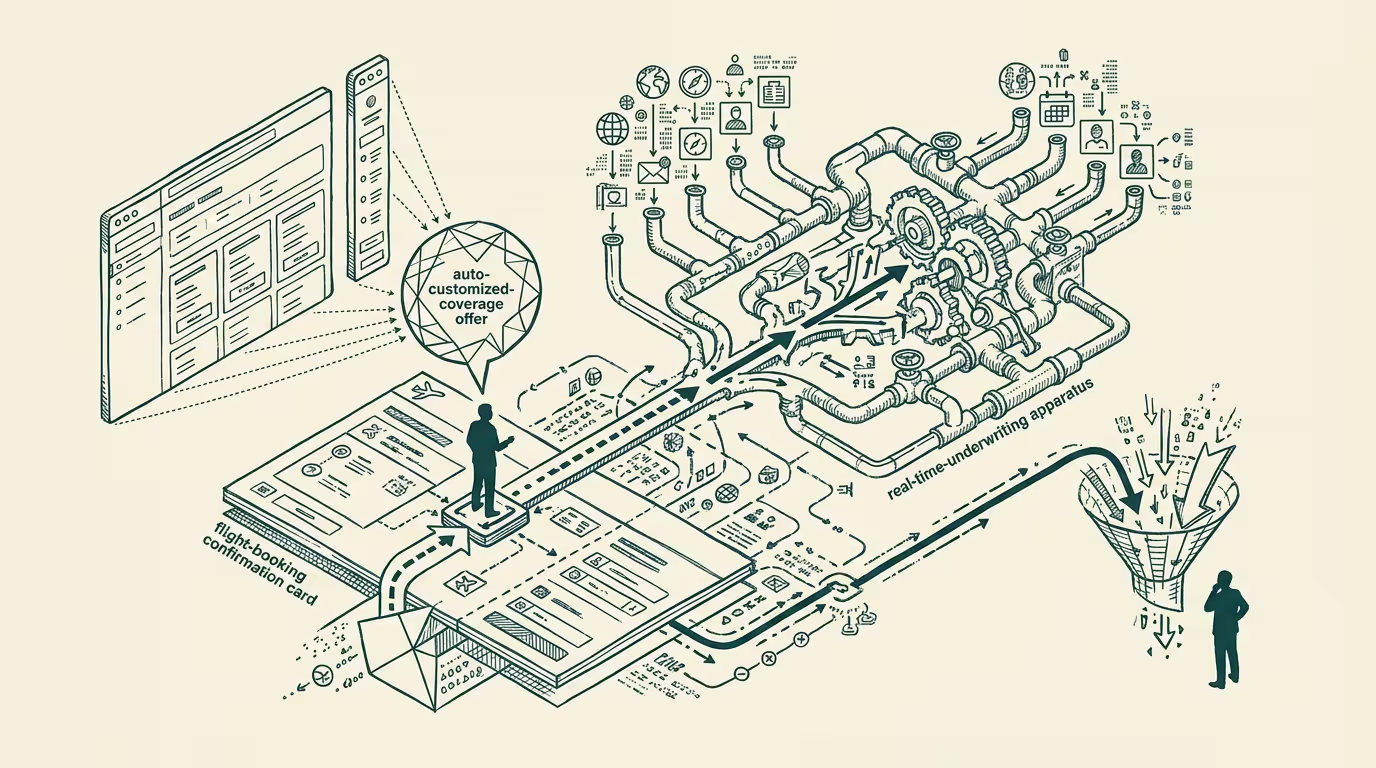

Booking became underwriting last winter.

The most underread travel-industry development of the last winter is not a route launch or a loyalty-program reset. It is that Allianz Partners, the world's largest travel-insurance provider by gross written premium, started firing an auto-customized coverage offer at the consumer inside a second of the flight booking confirmation. The mechanic is mundane on its face: a model reads the trip parameters as soon as the booking system commits the seat, prices a tailored policy against the destination, length, traveler profile, and recent claim distributions for the route, and pushes the quote into the booking-confirmation surface before the consumer has clicked through to the next page. Christopher Elliott reported the deployment in Forbes in early 2024, and the trade press framed it as a consumer-benefit story about faster, more relevant coverage. The consumer-benefit framing is true and it is not the interesting frame. The interesting frame is that the moment a flight booking commits is now the moment the underwriting committee meets, and the committee is software, and the consumer is in the room without knowing it.

That last part matters more than the speed. Pre-2024, travel-insurance distribution was a pull category: the consumer finished the booking flow, then either remembered to comparison-shop a few standalone providers or accepted the airline's bolt-on at checkout. The bolt-on conversion was bad enough that the standalone providers had a real comparison window, sometimes hours and often a day or two, between booking and trip. Standalones won most of the dollars because the in-flow bolt-on was a bad product and the consumer who cared about coverage was the consumer willing to spend ten minutes off-flow. That window now compresses to roughly zero. A consumer who would have comparison-shopped is anchored to a quote priced more sharply than the bolt-on, and the quote arrives before the comparison instinct fires. The first-quote anchor is the win. Standalones do not lose because the new product is dramatically cheaper. They lose because the new product is in the booking surface and the comparison product is on a different tab the consumer never opens.

Three structural reads follow from the mechanic, and they are the reads that matter for anyone trying to figure out where the dollars sit four or five years out.

Data integration is the precondition, not the model

The first read is that the technical achievement is not the pricing model. It is the data plumbing. A sub-second personalized travel-insurance quote requires the booking system, the underwriting model, the actuarial-history database for the route, and the consumer profile to all be reachable from a single session context that has roughly a hundred milliseconds of slack. The pricing model itself is straightforward in the technical sense: travel insurance has been actuarially well-understood for decades, and the model that prices a route-segmented policy from a known-good claim history is a small ML problem layered on a deterministic rate calculator. What was not solved before 2023 was the integration. The booking platform, the policy-issuance system, and the underwriting database were running on three different vendors, and the round trip was not measured in milliseconds. The Allianz-with-distribution-partner deployment works because the integration was rebuilt to run in a single context. The vendors that win the next round of this category will be the ones that hold the integrated context end-to-end, and the vendors that keep selling a separate quote-engine API will be priced into the floor.

This is the same structural lesson the operations side of healthcare keeps relearning, where the deployable products in pharmacy, scheduling, and imaging are not the ones with the cleverest model but the ones that ship inside the workflow the operator already runs. Travel-insurance distribution is now an integration story. The model is a small piece of it.

Integrated platforms displace standalone intermediaries

The second read is the displacement argument. Standalone travel-insurance intermediaries (the comparison sites, the niche brokers, the agency channel that has historically lived on the seven-to-twelve percent commission off the cruise- and tour-operator booking) have a structural problem that does not have a near-term answer. The integrated platforms, meaning the OTAs and the airline direct-booking surfaces and the credit-card travel portals that already hold the consumer at the booking moment, can offer underwriting at zero marginal cost of consumer attention. Standalone intermediaries cannot, because the consumer is not on their surface at the moment that matters. They can compete on price, but the price gap is not large: Allianz and its peers will route the in-flow distribution at a tighter margin than the comparison-shopping consumer would have extracted, and the integrated-distribution version sits at the moment of maximum behavioral commitment. They can compete on coverage breadth, and they will, but coverage breadth is not what the median traveler is buying when the trip is a four-night domestic flight with a checked bag. What the median traveler is buying is convenience and a defensible-against-claim policy at a defensible price, and the in-flow product is winning that comparison.

The remaining standalone segment, in this read, is the high-end and complex-trip business: the multi-leg international itinerary with cruise plus excursion plus ground component, the medical-evacuation-heavy expedition policy, the family with a pre-existing condition that needs a real underwriter to look at the case. That segment is real and is going to stay standalone for at least another decade because the in-flow models will not have the policy flexibility to handle it. But the volume business, which is most of the volume, walks into the integrated channel.

Wearables-to-underwriting is the next data layer

The third read is the futurist-adjacent one but it is grounded in the same data-integration precondition argument. Once the integrated platform is holding booking-intent data in the same session context as the consumer's profile, the next data layer the platform will reach for is the consumer's health-profile data. The reason is that travel-insurance underwriting has a known-good correlation between traveler-health signal and claim probability, and the historical underwriting could only access a coarse self-disclosed version of that signal at policy issuance. A platform that holds consented access to a continuous wearable feed (heart-rate variability, sleep regularity, activity baseline) prices the policy against a much sharper signal than the self-disclosure version, and the signal is more honest because the consumer cannot pencil-whip a smart-watch the way they can pencil-whip a pre-existing-conditions form. The first deployments will look like a discount for opted-in consumers with consistent activity baselines, which will read as consumer-friendly and will be hard to complain about. The structural effect is that wearable platforms become a commercial input into a non-clinical insurance pipeline, and the data-portability infrastructure that was built for clinical interoperability becomes a non-clinical commercial asset.

The competitive question for the wearable platforms is whether they sell that data layer as a B2B input to the integrated travel platforms, or whether they offer underwriting themselves and become the integrated platform. Apple and Google are the two operators with both the wearable footprint and the booking-adjacent surface (Apple Wallet, Google Travel) to attempt the second move. Whether they take it depends on regulatory appetite more than technical readiness. The technical pipeline is shovel-ready. The regulatory framework for wearable-data-priced insurance is not.

What to watch and what would falsify

Three things to watch through the back half of 2024 and into 2025. One, whether the comparison-site segment of the standalone market reports a measurable conversion-rate decline on volume policies during the same windows that the integrated-distribution deployments expand. The decline is the signal that the displacement argument is operating in the data and not just in the structural reasoning. Two, whether a wearable-feed-discounted travel-insurance product launches in any major market, not as a press-release pilot but as a posted product on a real distribution surface. The first such product is the moment the futurist read collapses into the present read. Three, whether any insurance regulator in a tier-one market opens a docket on real-time behavioral-trigger underwriting, because the docket is the lead indicator that the regulatory framework is about to cap the upside the part that holds is forecasting.

The argument falsifies cleanly on one shape. If the integrated-distribution deployments stall on consumer-conversion at numbers similar to the bolt-on era, the displacement is not happening and the standalones are safe. The deployment data so far does not suggest that shape, but the data is early. The read that survives is that the structural mechanism is in place, the first deployment is working, and the next two data layers are queued. The category that was distributed by comparison-shopping is going to be distributed by booking-context, and the category that priced on self-disclosure is going to be priced on telemetry. Both transitions are already underway. The travel side is six months ahead of the healthcare-data side. The travel side is also where the dollars move first, because the booking surface is where the consumer is standing.

Booking became underwriting last winter. The underwriting committee meets in software now, and the consumer joins it without being told. The next committee meeting will read the wearable feed.

—TJ