Booking vs. Expedia 2025: the OTA hierarchy just had its biggest single-year shift in 15 years.

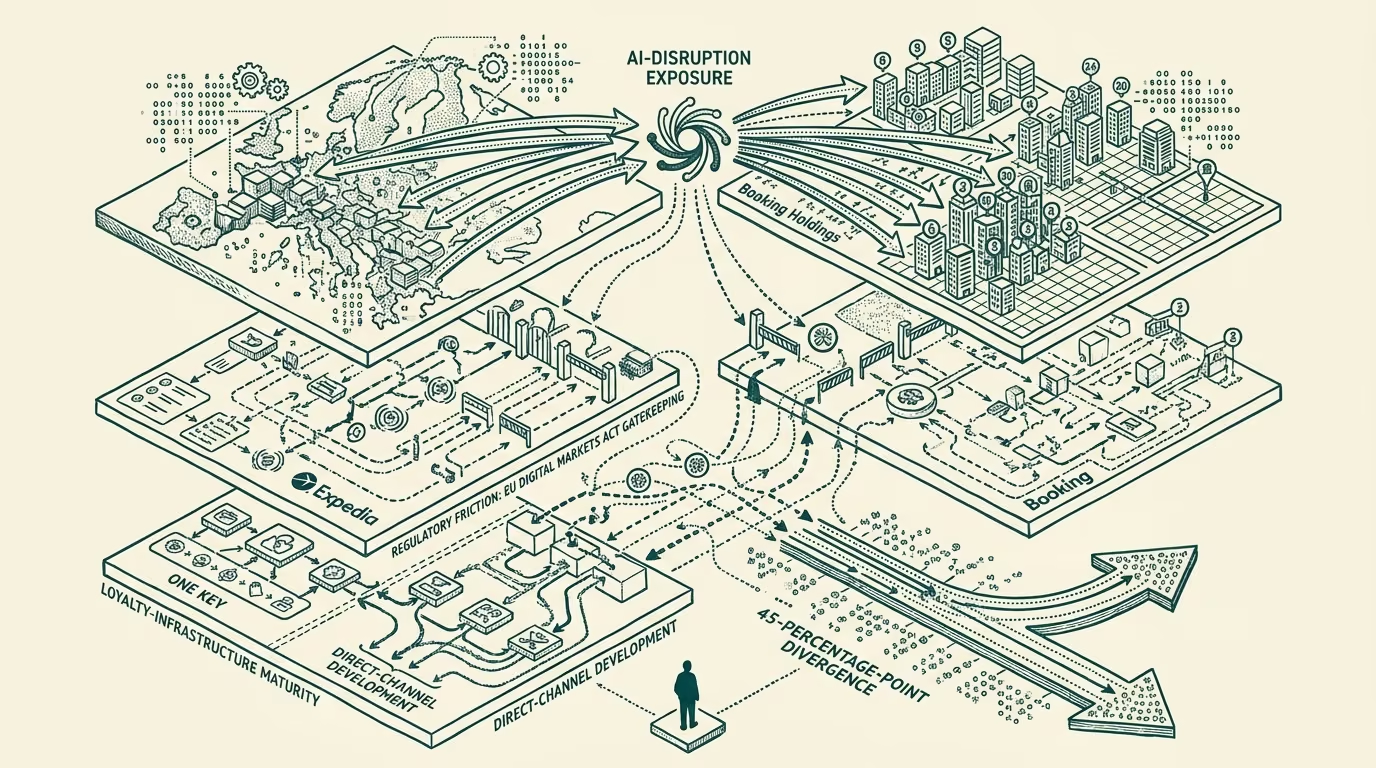

The 2025 stock-price returns at Booking Holdings and Expedia Group ran roughly 10 percent and 55 percent respectively, producing a roughly 45-percentage-point divergence between the two major OTAs in a single year. The divergence is the largest single-year hierarchy shift between the two companies since the early 2010s, when the post-financial-crisis recovery trajectories produced sustained valuation differentials between the two. The 2025 divergence is structurally different: it maps not to a recovery cycle but to differential exposure to the AI-Overview-and-Google-disruption pattern discussed elsewhere, differential European regulatory engagement, and differential OTA-strategy positioning the two companies have been running through 2024-2025.

Booking Holdings, the larger of the two and historically the higher-margin operator, ran into the AI-disruption exposure harder than Expedia did through 2025. The reason is structural. Booking's revenue mix is more concentrated on the European hotel-and-vacation-rental segment that the AI Overview hits hardest in the per-vertical analysis. Booking's loyalty-program-and-direct-channel infrastructure, while substantial, is less developed than Expedia's One Key program through the same period. Booking's regulatory exposure in the EU, including the various Digital Markets Act compliance requirements and the gatekeeper-class regulation that has been progressively binding through 2024-2025, has tightened in ways that affect the company's organic-and-paid-search economics in the European markets where it concentrates revenue.

Expedia Group, the smaller of the two and historically the lower-margin operator, has been positioned somewhat better against the 2025 trajectory. The Vrbo property-rental business has held up because the AI Overview produces less effective answers for property-rental queries than for hotel queries. The flight-vertical concentration in the Expedia mix is helpful because the AI Overview impact on flight queries is shallower than on hotel queries. The One Key loyalty-program work has been compounding through 2024-2025 in ways that the underlying engagement-and-retention metrics have validated. The U.S. regulatory environment, where Expedia is more concentrated, has been less aggressive than the EU regulatory environment where Booking is more concentrated.

The combined effect is that Booking's structural advantages from the 2010-2024 era (scale, supply-graph depth, take-rate-leverage) compounded into vulnerability to the 2025 disruption pattern. Expedia's structural disadvantages from the same era (smaller scale, narrower supply-graph, weaker take-rate-leverage) made it less exposed to the disruption pattern that hit the structural advantages hardest.

The hierarchy shift between the two companies is real but should not be over-read. Booking remains the larger and higher-margin operator in absolute terms; the 2025 divergence is a meaningful narrowing of the gap, not a reversal. Expedia's 55 percent return runs partially against a lower base; the same divergence in absolute dollar terms is smaller than the percentage suggests. The longer-cycle question is whether the 2025 dynamic continues, with Expedia continuing to close the gap as the AI-disruption pattern compounds, or whether Booking adapts its operating model fast enough to defend its position.

The durable read is that the AI-disruption-and-regulatory-exposure variables are now central to OTA-equity valuation in a way they were not through 2010-2024. The 2026 OTA equity research that does not foreground these variables is using a framework that the 2025 trajectory has invalidated. Investors evaluating the OTA category need to weigh the differential exposure of the two majors carefully, and the longer-cycle trajectory will be substantially driven by which of the two adapts more effectively to the structural environment that has, finally, become visible in the public-markets data.

The 2025 hierarchy shift is the largest in 15 years. The shift is structural. The next 24-36 months will produce additional confirmation or revision of the 2025 read. The OTA hierarchy is, for the first time in a long time, a question with an open answer.

—TJ