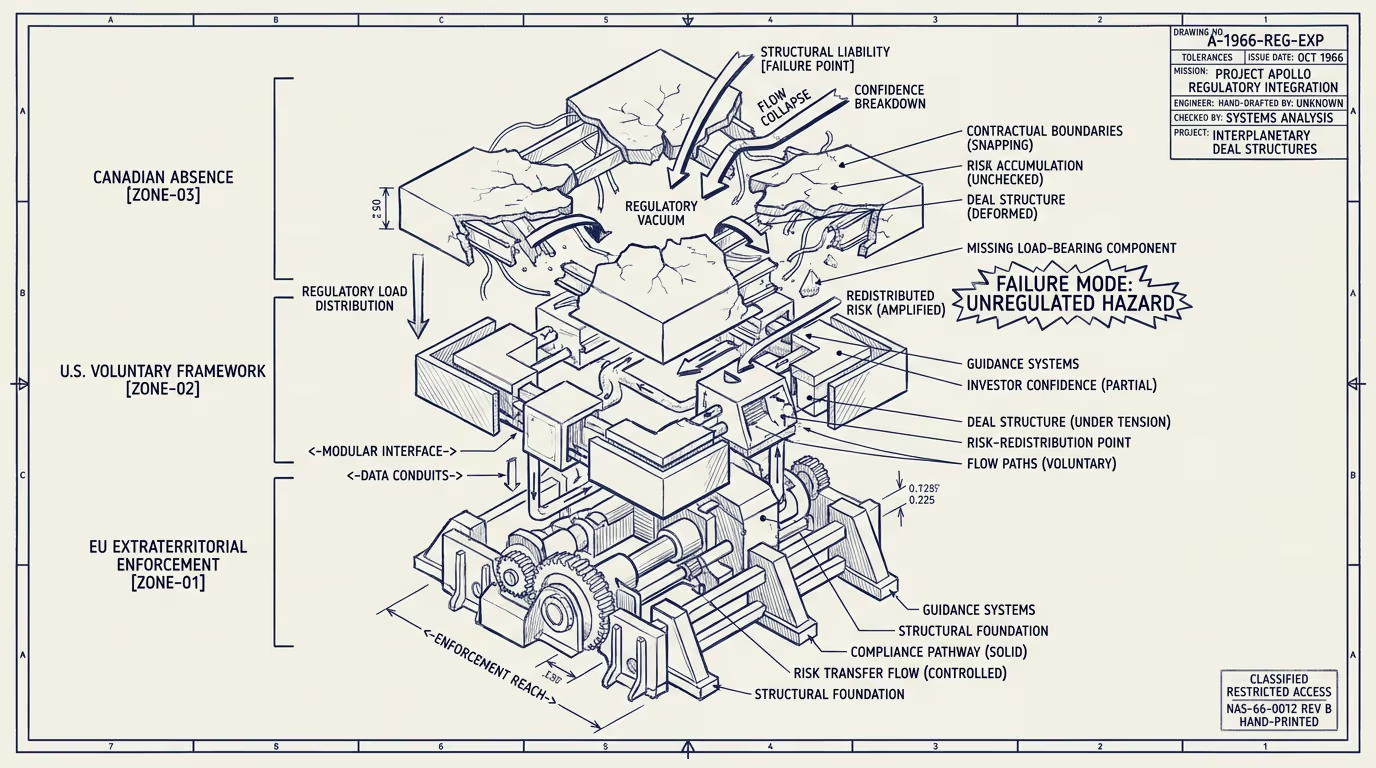

Canada's AI regulatory vacuum is not a feature. It is a liability at the investor table.

The Artificial Intelligence and Data Act died with Parliament in January 2025. AIDA had been the federal government's primary AI-regulatory vehicle, working through committee since 2022 with substantial amendment work but with the legislative process having taken longer than the political window allowed. When Parliament was prorogued in January 2025, the bill died on the order paper. The federal government's options for re-introducing it through the subsequent legislative session were politically constrained, with the result that Canada entered 2025 without a federal AI-regulatory framework and without a near-term legislative path to one.

The structural read on the vacuum is sometimes framed as an advantage for Canadian AI operators. The framing is wrong. The vacuum is a liability at the investor table, not a freedom-to-build feature, and the dollar cost of the liability is real. This essay walks the vacuum's shape, the cost mechanisms at the deal table, what Canadian operators should do about it, and the longer-cycle implication.

What the vacuum looks like

Through 2024-2025 the international AI-regulatory environment matured along two visible tracks. The EU AI Act came into force progressively through 2024-2026, with the high-risk-AI provisions applying to systems deployed in the EU regardless of where they were built. Canadian AI products that touch EU customers (which is most Canadian AI products that aspire to international markets) fall under the EU AI Act's extraterritorial reach. The U.S. ran a voluntary-framework approach centered on the NIST AI Risk Management Framework, the executive-order-and-state-level regulatory patchwork, and selected enforcement actions through agencies like the FTC, with the result that U.S. operators have a non-binding-but-substantive regulatory expectation against which to position their products.

Canadian operators have neither a domestic regulatory framework to point to nor the regulatory clarity that international frameworks provide their U.S. and EU peers. The Canadian operator pitching to a U.S. or EU investor cannot say "we are compliant with the Canadian framework" because the Canadian framework does not exist. The operator can say "we comply with the EU framework where applicable" or "we follow the U.S. NIST framework voluntarily" but those statements do not have the force of a domestic regulatory posture.

The vacuum is also visible at the procurement layer. U.S. and EU enterprise buyers evaluating Canadian AI vendors increasingly ask about the vendor's regulatory framework. The Canadian vendor without a clear answer to that question is structurally disadvantaged against U.S. and EU competitors who can point to their domestic framework.

The dollar cost at the deal table

The dollar cost of the regulatory vacuum surfaces at three points in the operator-class deal cycle.

The first point is at the Series-A-and-later funding cycle. Sophisticated investors evaluating AI-and-healthcare investments ask about the regulatory framework as a standard diligence item. The Canadian operator's answer to this question is structurally weaker than the U.S. or EU operator's answer, and the resulting valuation discount runs in the range of 10-25 percent depending on the specific category and the investor's regulatory-sensitivity. The discount is not always made explicit; it surfaces as a lower-than-expected pre-money valuation, more restrictive deal terms, or longer due-diligence timelines.

The second point is at the international-customer-acquisition cycle. EU and U.S. enterprise buyers running their procurement-and-compliance-review process favor vendors with clearer regulatory posture, with the result that Canadian vendors lose enterprise deals or accept longer sales cycles to address the regulatory-clarity gap. The cost runs as foregone revenue plus extended sales-cycle expense, with both being substantial for mid-market and larger Canadian AI vendors.

The third point is at the talent-acquisition cycle. Senior AI-and-healthcare engineering and product talent increasingly evaluate prospective employers against the regulatory-clarity question, particularly engineers and product leaders who have lived through compliance-class work in their prior roles. Canadian companies recruiting against U.S. and EU competitors are structurally disadvantaged on this dimension, with the cost surfacing as either lost talent or compensation premiums to overcome the regulatory-clarity gap.

The combined cost across the three points is meaningful in dollar terms. Canadian operators raising in 2025 are absorbing some combination of valuation discount, foregone international revenue, and talent-acquisition friction that their U.S. or EU peers are not absorbing.

What Canadian operators should do

For Canadian AI-and-healthcare operators reading the regulatory vacuum carefully, the practical advice runs along several lines.

The first practical line is to adopt international frameworks proactively. Canadian operators that publicly commit to the EU AI Act risk-classification-and-compliance posture, with documented compliance work and audit-able processes, can substantially close the regulatory-clarity gap with U.S. and EU competitors. The compliance work is meaningful, but the deal-table benefit is also meaningful, and most Canadian operators would do this work eventually anyway as their international customer base grows.

The second practical line is to engage with the standards-and-certification ecosystem that has emerged in the U.S. and internationally. Certifications under frameworks like the NIST AI RMF, the ISO 42001 AI management standard, the various sector-specific AI compliance certifications: these provide structured evidence of regulatory-class posture that Canadian operators can present to investors and customers. The cost of the certifications is meaningful but the deal-table benefit makes the ROI strongly positive.

The third practical line is sector-specific provincial-or-federal engagement. Healthcare-AI operators can engage with Health Canada and the provincial health regulators on AI-specific topics through the existing medical-device-regulation framework, even without AIDA. Financial-services-AI operators can engage with OSFI, the Bank of Canada, and the provincial financial regulators. The sector-specific engagement does not produce the comprehensive framework that AIDA would have, but it does produce defensible sector-specific regulatory posture that investors and customers can evaluate.

The longer-cycle implication

The longer-cycle implication of the AIDA failure is that Canadian AI operators are operating in a regulatory environment that is durably weaker than their U.S. and EU peers' environment for at least the next 24-36 months, with the timeline depending on whether and when the federal government re-introduces AIDA-equivalent legislation under the next political configuration. The 24-36 month timeline produces compounding effects on the Canadian AI ecosystem: less capital, slower international expansion, harder talent acquisition, and a structural disadvantage that grows with the duration of the vacuum.

For Canadian operators planning multi-year strategy, the practical advice is to plan against the durable vacuum scenario rather than the imminent-legislation scenario. Operators who plan against imminent-legislation will be disappointed when the legislation does not arrive. Operators who plan against the durable vacuum will be positioned to absorb the cost and continue building, with the international-framework adoption and the certification-ecosystem engagement as the substitution for domestic regulatory clarity.

Canada's AI regulatory vacuum is not a feature. It is a liability with a measurable cost at the investor table and the customer table and the talent table. Canadian operators who recognize the cost and address it through international-framework adoption and sector-specific engagement will close the gap meaningfully. Operators who treat the vacuum as freedom-to-build will continue to absorb the cost without naming it. The vacuum is not going away soon. The cost is real. Build accordingly.

—TJ