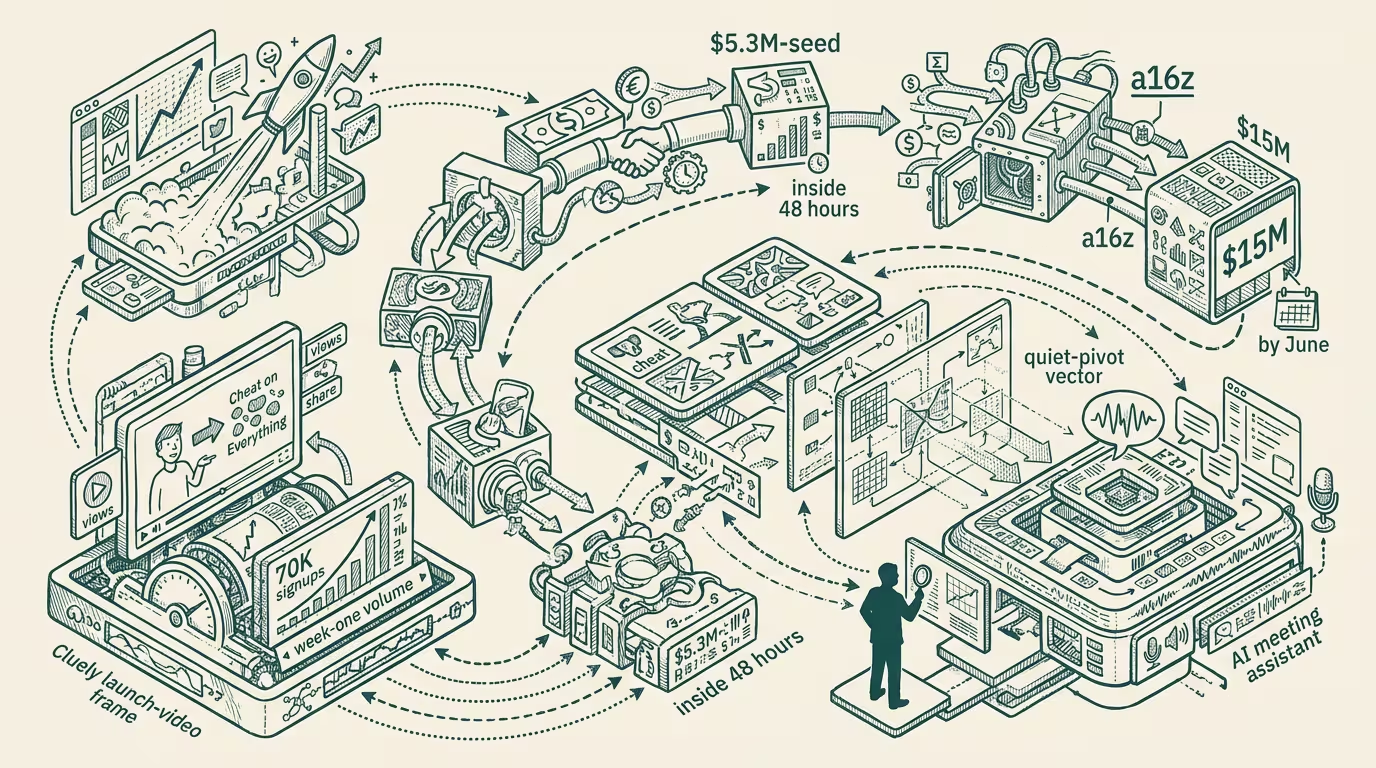

Cluely raised $5.3M for a posture. The posture became the category.

Roy Lee launched Cluely on April 20, 2025, with a video titled "Cheat on Everything." The product was framed as an undetectable AI overlay for job interviews, sales calls, and exams. The launch drew 70,000 signups in week one. A $5.3M seed closed inside forty-eight hours. By June 2025, a16z had led a $15M Series A. By August, the company had quietly repositioned as "Cluely, AI meeting assistant." The cheat-on-everything framing receded.

The trade press read the arc as either a viral-marketing case study or an ethics scandal. Both readings miss the durable read.

The durable read is that the launch posture became a venture-bankable category before the product caught up.

Walk through the mechanism. Roy Lee picked a posture (cheating-as-product) that got attention. The attention drew signups. The signups produced a venture-class data point — 70K signups in week one is a top-decile launch metric for any category. The venture-class data point produced the $5.3M seed. The seed produced the $15M Series A. By the time the $15M closed, the company had pivoted to a category (AI meeting assistant) that existed at scale. The pivot let the company keep the venture funding and shed the posture.

_The posture was the wedge. The category was the destination. The interim was the venture-class commitment._

Was the arc deliberate or emergent? Lee's public posture suggests deliberate. The pace of the pivot suggests deliberate. But the deliberateness is not the operator-relevant tell. The operator-relevant tell is that the playbook works.

What's the structural shift the playbook represents? Pre-2024, the venture-class read on a posture-driven launch was that the posture was a distraction from the product. The Cluely arc inverts that read. The posture is the distribution. The product is the destination. The venture investor commits to the trajectory rather than to the launch product. The pre-Cluely framing valued product-readiness; the post-Cluely framing values posture-distribution. The shift is, in operating terms, a category-creation event for venture-class allocation.

What's the operator-class skill that makes the playbook work? Pivot timing. Lee pivoted Cluely from cheat-on-everything to AI-meeting-assistant within four months of launch. The pivot was, in operating terms, well-timed — late enough to capture the attention round, early enough to avoid being defined by the controversy. Operators running similar arcs in adjacent categories have to manage the pivot timing precisely. Pivot too early and the attention round capital does not commit; pivot too late and the venture-class commitment is constrained by the original posture.

What's the press getting wrong? The trade press wrote up the controversy. The venture press wrote up the funding. Neither wrote up the structural shift in venture-class allocation patterns that the Cluely arc represents. The structural shift is that posture-as-distribution is now a fundable launch model, and the bar for venture commitment is lower than it was eighteen months earlier. Operators who recognize the shift can either run the playbook or position against it. Operators who treat the Cluely arc as a one-off are missing the category-creation event.

The same shape recurs across categories. In healthcare, the analogous arc is the wellness-influencer-pivots-to-clinical play (the posture is wellness; the destination is regulated clinical; the venture-class commitment funds the pivot). In travel, it is the loyalty-status-influencer-pivots-to-points-platform play. In B2B SaaS, it is the controversial-thought-leader-pivots-to-platform play. Each category has its own posture, its own destination, and its own pivot timing.

AI startups specifically run the posture-as-distribution play more cleanly because the underlying category is moving fast enough that the destination doesn't have to be defined at launch. In a slow-moving category the pivot is constrained by the existing market structure. In AI, the market structure is rebuilding monthly, so the pivot has flexibility that adjacent categories don't. That flexibility is the operating-leverage Lee captured.

Cut through the trade-press framing and the picture sharpens. Cluely is the cleanest visible case study of a launch-posture-becomes-category arc, the venture-class read on the arc is durable enough that the playbook will recur, and the structural read is to recognize the play when adjacent companies run it. By 2027 the playbook will have a name in the venture-class lexicon. The name will, of course, be coined by whoever runs the next iteration most successfully.

The honest follow-up is that the repositioning to AI meeting assistant placed Cluely in a crowded category (Otter, Fireflies, Granola, Read.ai). The venture-class commitment funded the entry. Whether the company captures category share against the entrenched competitors is the next eighteen-month question. The answer to that question is the actual product question. The launch posture got Cluely the funding. The product question gets it the company.

Lee raised $5.3M for a posture. The posture became the category. Whether the category becomes the company is, in operating terms, the part that the launch theatrics could not accelerate.

—TJ