Culture is downstream of structure. Southwest's Elliott settlement is the evidence.

Southwest Airlines settled with Elliott Investment Management in October 2024 after a multi-month activist campaign. The settlement produced six new directors on the Southwest board, an operational-and-strategic-review process that has produced substantial changes through 2024-2025, and a public acknowledgment that the carrier's strategic posture had drifted from competitive viability. The most visible operational change has been the announced end of the 60-year open-seating policy, with assigned-seating implementation ramping through 2025-2026. The premium-cabin and red-eye-flight rollouts that the carrier had resisted for decades are also moving into deployment.

The trade-press coverage of the settlement focused on the cultural change. The Southwest way, which had been the carrier's marketing positioning and the press-friendly story for decades, was finally giving way to the boring operational realities the rest of the industry had adopted. The framing treated the cultural change as the substantive story.

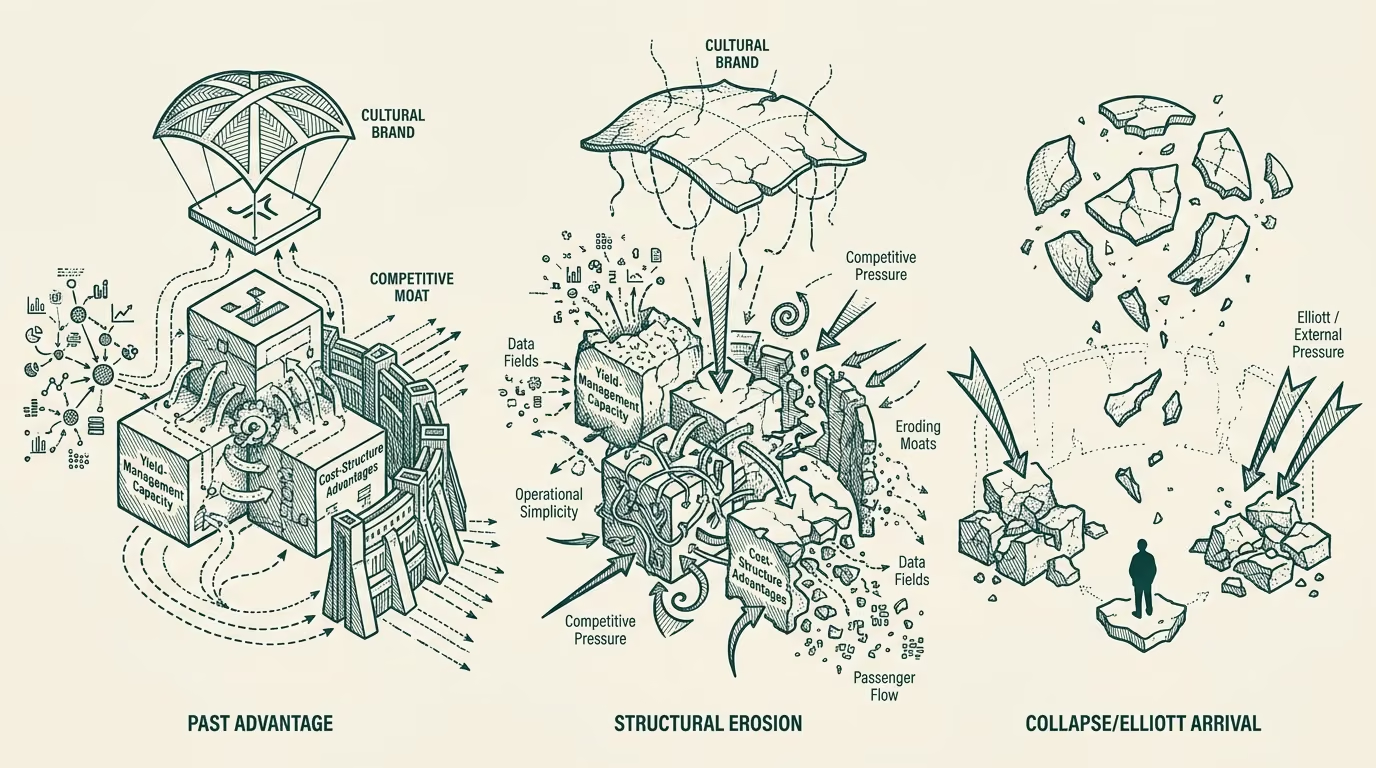

The substantive story is structural, not cultural. Southwest's competitive position had eroded for several years before Elliott arrived, and the erosion happened on dimensions that the cultural framing had been obscuring. The yield-management capacity, the operational simplicity, and the cost structure that produced the carrier's actual moat had compressed. The culture was the surface presentation that the structural moats supported. When the structural moats compressed, the cultural surface had nothing underneath it. The Elliott settlement is the visible moment when the structural reality became impossible to ignore.

This essay walks the durable read.

What the actual moats were

Southwest's structural moat through the 1970s-2010s ran on three reinforcing axes. The yield-management-and-pricing capability allowed the carrier to operate at unit revenues that beat its cost structure on the leisure-leisure routes the carrier prioritized. The operational simplicity (single fleet type, point-to-point network, no interline coordination, no premium-cabin complexity) produced unit costs that were structurally below the legacy carriers' costs. The labor-and-cost structure was favorable, partly through the carrier's specific labor-relations history and partly through the operational simplicity that reduced the labor-coordination cost across the network.

The combined effect was that Southwest could operate against the legacy carriers on the leisure-leisure segment with a cost-and-revenue structure that produced sustainable margin where the legacy carriers struggled. The cultural framing (the Southwest way, the customer-friendly attitudes, the open-seating egalitarianism) was the marketing surface that the structural advantages allowed the carrier to maintain. The marketing surface was real and operationally observable, but it was downstream of the structural advantages, not the cause of them.

What changed

Through 2015-2024 the structural advantages compressed in several ways. The other major U.S. carriers improved their unit-cost structures through a combination of operational improvements, more sophisticated yield management, and continued labor-cost discipline. The fuel-cost advantages that Southwest had captured through aggressive hedging in the 2000s and early 2010s did not persist into the late 2010s. The fleet-cost advantages that came from operating a single 737-family fleet became less distinctive as the legacy carriers also concentrated their fleets. The leisure-leisure-route advantage that Southwest had on the routes the legacy carriers under-served compressed as the legacy carriers and the ULCCs filled in those routes.

The result by 2020-2023 was that Southwest's cost structure was no longer meaningfully advantaged against Delta, United, and American on the routes Southwest cared about. The yield-management-and-pricing advantage had compressed. The operational-simplicity advantage was smaller because the legacy carriers had improved on this dimension. The labor-cost position was approaching parity with the legacy carriers' positions.

The cultural surface continued to be presented (the Southwest way, the customer-experience differentiation) but the structural advantages that had supported the surface had compressed. The carrier was operating closer to commodity-airline economics with a marketing-class differentiation that the operational reality could no longer back up.

What Elliott actually surfaced

Elliott's activist position made the structural reality public. The arguments Elliott pressed (assigned seating, premium-cabin offerings, red-eye operations, network restructuring, board renewal, leadership change) were operational arguments for converging Southwest's operating model toward the rest of the industry. The arguments were correct in operational terms. They were also a public acknowledgment that the cultural-framing era was over and that the carrier needed to operate as the boring legacy-class carrier its structural position now required.

The settlement did not change Southwest's structural advantages, because there were no structural advantages left to change. The settlement changed the cultural surface to match the structural reality. The carrier going forward will operate with assigned seating, premium cabins, red-eye flights, and the broader operational complexity the legacy carriers operate with. The structural margin profile is going to look more like the legacy-class margin profile, with the cultural-differentiation premium having mostly evaporated.

What this implies

The structural lesson for the operator class is that culture is downstream of structure. Operating businesses that present a cultural-differentiation story alongside a structural-advantage story can sustain the cultural-differentiation as long as the structural-advantage holds. When the structural-advantage compresses, the cultural-differentiation has nothing underneath it and the cultural-differentiation either erodes naturally or is forced to converge by activist pressure or by competitive pressure or by the financial reality of the compressed margins.

The lesson generalizes beyond Southwest. Operators in any category running cultural-differentiation strategies should evaluate whether the underlying structural-advantage is durable. If the structural-advantage is durable, the cultural-differentiation can be sustained. If the structural-advantage is compressing, the cultural-differentiation will follow on a multi-year delay. Investors evaluating cultural-differentiation strategies should price the structural-advantage trajectory rather than the cultural-presentation, because the cultural-presentation is downstream and lagging.

For travel-industry operators specifically, the Southwest case is the cautionary template. Carriers presenting cultural-differentiation framings (the JetBlue customer-experience story, the Alaska community-and-route-differentiation story, the various international-carrier brand stories) should be evaluated against their structural-advantage trajectories. The carriers whose structural advantages are compressing will, in their own time, see the cultural framings forced to converge by structural reality.

The Southwest way was never the moat. The moat was the unit economics, the operational simplicity, and the yield-management capability. When those compressed, the moat was gone, and the cultural framing had nothing left to defend. Elliott surfaced the structural reality publicly. The settlement is the visible moment. The longer-cycle implication for the operator class is that cultural-differentiation strategies need a structural-advantage foundation, and when the foundation compresses the strategy follows. Build for the structure. The culture follows the structure, not the inverse.

—TJ