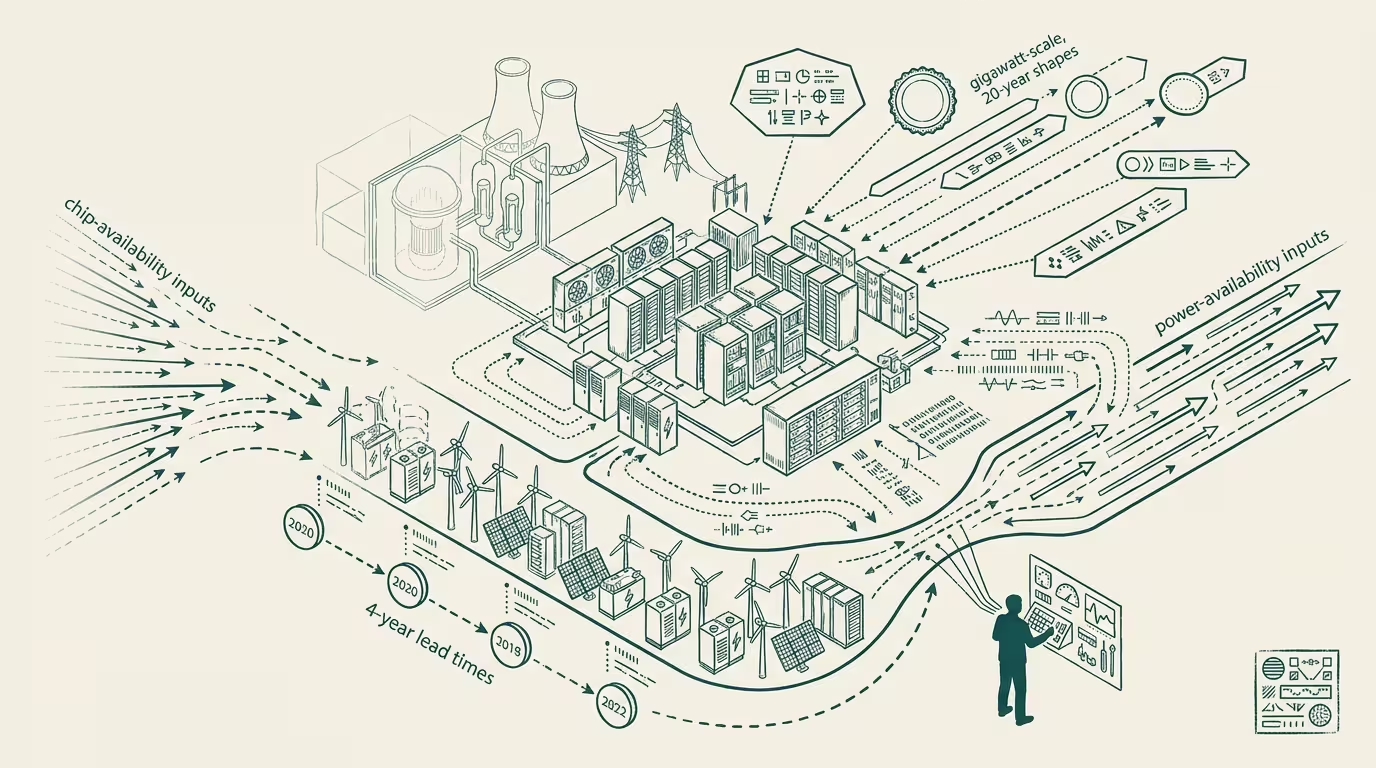

Energy is the new chip. The grid is the four-year overhang.

Through 2024 the AI-infrastructure narrative was about chips. Nvidia capacity, TSMC fab allocation, the H100-to-Blackwell transition, the export-control regime around advanced fabrication. By late 2024 the narrative had shifted. The Microsoft-Constellation 20-year, 835MW PPA to restart Three Mile Island Unit 1 (announced September 2024) made the shift visible at the trade-press layer. The AI-data-center site-selection map inverted from "near-fab availability" to "near-power availability." Hyperscaler PPAs at gigawatt scale became the operating-relevant procurement question.

_Energy is the new chip. The grid is the four-year overhang._ Hold that frame in view. Everything that follows traces back to it.

The compute-energy coupling closed in 2024. Pre-2024, the binding constraint on AI-infrastructure scaling was chip availability. Post-2024, the binding constraint is grid interconnection queues — the multi-year delays in connecting new data-center loads to regional electrical grids. The Princeton ZERO Lab and other grid-analysis groups documented interconnection-queue wait times averaging 4-5 years across most U.S. ISOs as of 2024-2025. The wait-time dynamic produces a four-year overhang during which the operators with locked-in power positions capture asymmetric infrastructure leverage.

This is, in operating terms, a futurist forecast piece. The forecast is conditional on the queue-time dynamic continuing on its current curve, the political-economy class continuing to prioritize regulatory-streamlining for AI-class loads (which is uncertain), and the technology-class not producing a step-change improvement in compute efficiency that would compress aggregate energy demand. If those conditions hold, the four-year overhang is durable through approximately 2028-2029. If they don't, the overhang compresses faster.

Trace the overhang back to power-procurement and the new fab-allocation surfaces. Operators with locked-in multi-year PPAs at gigawatt scale capture infrastructure leverage that operators without those agreements cannot replicate inside the queue-time window. Microsoft's Three Mile Island deal, Amazon's Talen Energy partnership, Google's various nuclear-and-renewable agreements through 2024-2025 — each is a power-procurement position that, in the four-year overhang, is more strategically valuable than the chip-procurement positions of the same scale. Operators tracking the AI-infrastructure procurement landscape should be tracking power-procurement deals at the same fidelity they track GPU-allocation announcements.

Trace the overhang back to grid-adjacent-real-estate and the new fab-adjacent-real-estate surfaces. Pre-2024 the AI-infrastructure real-estate map was dominated by Northern Virginia, Silicon Valley, and Dublin (proximate to fab supply chains). Post-2024 the map adds locations dominated by power availability — Texas (ERCOT permissive interconnection), Iowa and Nebraska (wind capacity plus grid headroom), the Pacific Northwest (hydro plus historical data-center clusters). The real-estate-class capital allocation that follows the inversion is operationally visible by Q3 2025 and accelerates through the overhang period.

Trace the overhang back to regulatory-streamlining and the operator-class lobbying priority surfaces. The pre-2024 regulatory-class engagement on AI infrastructure was fab-export-control and chip-supply-chain. Post-2024 the engagement adds grid-interconnection-queue management — federal and state permitting reform, PJM and ERCOT queue-prioritization rules, the FERC-class transmission-policy work. The operator class that captures regulatory-class wins on these questions captures asymmetric advantage in the overhang. The operators not engaging with the regulatory-class are paying the queue-time cost without compensating regulatory leverage.

The same pattern recurs across categories beyond AI-infrastructure. Crypto-mining (already on the curve, similar interconnection-queue dynamics). Industrial-electrification (slower curve, different regulatory environment). EV-charging-infrastructure (different scale, similar grid-side-interconnection mechanics). Each category has its own version of the four-year-overhang dynamic, and each has its own operator-level adaptation.

The forecast is contingent on the political-economy of grid policy not producing a step-change response. The contingency cuts both ways. If the federal government runs an explicit "grid expansion is national strategic priority" frame (analogous to the chip-fabrication frame established by CHIPS Act), the queue-time dynamic compresses faster than the four-year overhang implies. If the political-economy class continues to under-prioritize grid expansion, the overhang extends. The 2026-2028 election cycles will, in practice, decide which scenario plays out.

What survives all of this is that the energy-as-the-new-chip framing is one of the cleaner futurist-class observations of 2024-2025, the four-year-overhang forecast is contingent on the queue-time dynamic and the political-economy environment, and the operator discipline is to position power-procurement, grid-adjacent-real-estate, and regulatory-class engagement as first-tier infrastructure questions rather than as adjacent considerations to chip-procurement. Operators running the three primitives explicitly are positioned for whichever scenario plays out. Operators running 2023-shape AI-infrastructure plans against 2026-shape constraints are operating against a binding constraint they did not price.

Energy is the new chip. The grid is the four-year overhang. The forecast cuts both ways depending on the political-economy class's response. Operators with positions across the three primitives are operating-coherent in either direction. The overhang is, in either direction, the operating reality of the next thirty-six to forty-eight months.

—TJ