The GDS will outlive every startup that came to disrupt it. American Airlines paid $1.5B to prove it.

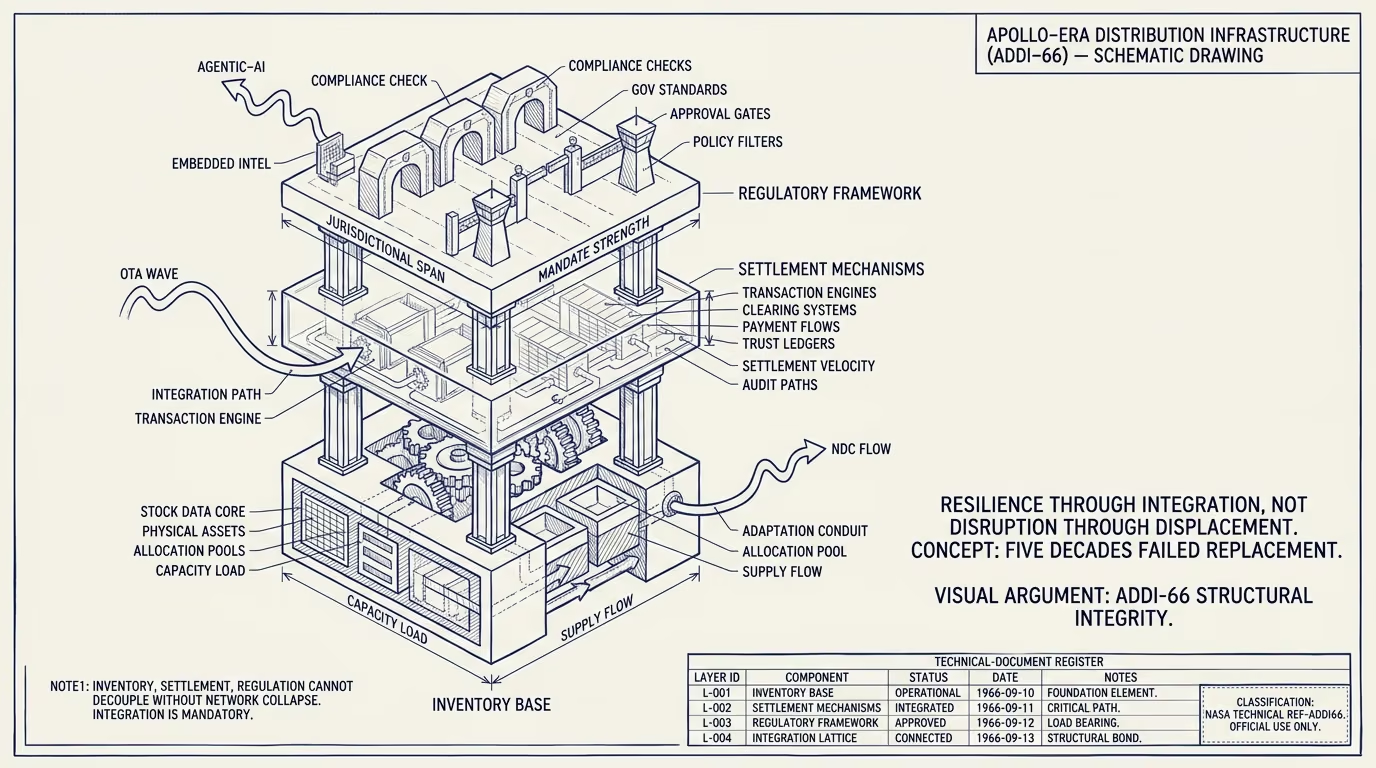

The Global Distribution Systems (Amadeus, Sabre, Travelport) emerged in the mid-1970s as airline-owned reservations infrastructure, were spun out into independent companies through the 1990s, and have been the backbone of multi-supplier airline distribution for half a century. Every wave of disruption since has assumed that the GDS infrastructure was about to be replaced. The 1990s online-booking wave assumed the GDS was a relic of the agency-tier era. The 2000s OTA wave assumed the GDS was about to be displaced by direct-OTA-to-airline integrations. The 2010s NDC wave assumed the GDS was about to be replaced by airline-direct API distribution. The 2020s agentic-AI wave is currently assuming the GDS is about to be made irrelevant by autonomous-routing-and-booking agents.

Each prediction has been wrong on the timeline that mattered. The GDS infrastructure has absorbed each disruption wave, integrated the new distribution mechanism alongside the legacy one, and continued to carry the bulk of the airline-distribution traffic. American Airlines' approximately $1.5 billion in settlement, customer-service-recovery, and revenue-loss costs from its 2023-2024 attempt to push hard on the NDC-and-direct-distribution strategy and back away from the GDS is the visible 2025 signal that the GDS infrastructure is stickier than the disruption-class operators continue to assume.

This is a forecast piece. The intent is to walk the fifty-year pattern, name the three structural reasons the GDS pattern persists, identify the one structural reason that eventually breaks the pattern (and on what timeline), and lay out what the part that holds on the next decade should be.

The fifty-year pattern

The pattern starts in 1976 with American Airlines launching the Sabre system as in-house reservations infrastructure for the carrier's own travel agencies and passenger-service operations. The other major U.S. and European carriers followed (United's Apollo, TWA's PARS, Air France-Lufthansa's Amadeus consortium). Through the 1980s the carrier-owned reservations systems became the multi-carrier distribution backbone, with travel agencies using the GDS terminals to book inventory across carriers. The systems were spun out from carrier ownership through the 1990s and consolidated into the three-pole structure (Amadeus, Sabre, Travelport, with Worldspan and Galileo eventually consolidating into the Travelport pole).

The 1990s online-booking wave assumed the GDS was about to be bypassed because the consumer-facing direct-booking channels would let consumers book directly with the airline. What actually happened is that the consumer-facing direct-booking channels also ran on top of GDS infrastructure, with the OTAs and the direct-booking sites both querying GDS-mediated inventory. The GDS absorbed the new channel rather than being bypassed.

The 2000s OTA wave assumed the GDS was about to be displaced by OTA-to-airline direct integrations, which would route around the GDS layer and reduce the take rate the GDS extracted from the bookings flowing through. Some direct integrations did happen. The volume that moved off the GDS was meaningful but bounded, and the GDS continued to carry the majority of the agency-and-OTA distribution.

The 2010s NDC wave assumed the GDS was about to be replaced by airline-direct API distribution under the IATA NDC standard. The replacement did not happen, as discussed in the NDC piece. The GDS-NDC translation layer became the de facto integration pattern, with the GDS continuing to carry the volume.

The 2020s agentic-AI wave is currently assuming that autonomous-AI agents will route bookings outside the GDS infrastructure, with the agents querying carriers directly. The early evidence is that the agents query the carrier-direct APIs where they exist and fall back to GDS-mediated inventory where they do not, with the result that the GDS continues to carry the bulk of the agentic-AI-driven volume too.

The pattern is consistent. Each disruption wave assumed displacement and produced absorption. The GDS infrastructure remains.

The three structural reasons the pattern persists

Three structural reasons explain why the GDS infrastructure has absorbed every disruption wave rather than being displaced.

The first reason is inventory aggregation. The GDS holds the multi-carrier inventory in a single queryable structure, with the airlines pushing schedule, fare, and availability data into the GDS in real time. A new distribution channel that wants to offer multi-carrier inventory either has to integrate with the GDS to get the inventory or has to build its own multi-carrier integration layer that replicates what the GDS already does. The replication is engineering work that takes years and produces a result that is, at best, equivalent to what the GDS provides. The economic case for replication is weak, and most disruption attempts end up integrating with the GDS rather than replacing it.

The second reason is settlement infrastructure. When a travel agency or OTA books a flight through the GDS, the financial settlement (the payment from the consumer, the commission to the agency, the take rate to the GDS, the net to the airline) flows through the GDS-mediated settlement infrastructure (the Airline Reporting Corporation in the U.S., the Billing and Settlement Plans through IATA elsewhere). The settlement infrastructure has been built up over decades, has integrations with thousands of agencies and dozens of carriers, has compliance-and-audit posture for the regulatory requirements, and has insurance-and-liability structures that protect the participants. A new distribution channel that wants to bypass the GDS has to either integrate with the existing settlement infrastructure (which still flows through the GDS) or build a replacement (which has to clear the same regulatory-and-compliance bar). The replacement work is multi-year and expensive.

The third reason is regulatory posture. The GDS-and-settlement-infrastructure ecosystem has cleared decades of regulatory review across the major jurisdictions, with the operating rules, the consumer-protection requirements, the antitrust postures, and the contractual structures all having been negotiated against the regulators. A new distribution channel that operates outside this ecosystem has to clear the regulatory bar independently, which slows the deployment and adds risk. Most disruption attempts have not been willing to absorb the regulatory ramp.

The three reasons reinforce each other. The inventory aggregation is what makes the GDS valuable to the agency-and-OTA tier. The settlement infrastructure is what makes the GDS reliable for the carrier-and-payment side. The regulatory posture is what makes the GDS durable across jurisdictional changes. A disruption attempt that addresses one of the three but not the other two does not displace the GDS; it adds a parallel layer that the GDS absorbs.

The American Airlines $1.5B receipt

American Airlines pushed hard on the direct-distribution-and-NDC strategy through 2023-2024, attempting to redirect agency-and-OTA bookings from the GDS-mediated channel to the carrier-direct channel. The strategy ran into the structural reasons described above. Agency-tier customers preferred the GDS-mediated booking flow because the workflow was already there. Settlement-side complications meant that the direct-channel bookings carried friction the GDS-mediated bookings did not. Regulatory and contractual issues with the DOJ's antitrust review of major carrier behaviors added further constraints.

By mid-2025 the carrier had retreated substantially from the strategy, with public commentary acknowledging that the cost of the direct-distribution push had run into roughly $1.5 billion in settlement, customer-service-recovery, agency-rebate, and revenue-loss expense. The carrier did not abandon NDC entirely but pulled back from the aggressive-displacement posture and returned to a hybrid model where the GDS continues to carry the bulk of the volume.

The American Airlines receipt is the most expensive recent demonstration that the disruption-against-GDS pattern produces a pattern of partial displacement and substantial cost. Other carriers have run smaller versions of the same experiment with similar results. The GDS infrastructure has absorbed the experiments and the carriers have, eventually, returned to the GDS-mediated pattern.

The structural reason that eventually breaks the pattern

The one structural reason that does eventually break the GDS pattern is the technology-and-cost trajectory of the underlying inventory-aggregation function. The GDS infrastructure runs on legacy technology stacks (much of the core inventory-and-pricing logic dates to the 1970s-1980s, with successive layers of modernization on top), with cost structures that reflect the legacy architecture. The cost-to-rebuild the inventory-aggregation function on a modern technology stack is decreasing year over year as the engineering capacity for distributed-systems work, the cost of compute, and the availability of pre-built integration tooling improve.

There is a forecast horizon at which the rebuild becomes economically viable. The horizon is moving closer through the 2020s but is unlikely to land within the next decade for the reasons above (settlement infrastructure, regulatory posture). The forecast for when a credible GDS-replacement actually emerges is somewhere in the 2032-2040 window, with substantial uncertainty in the exact timing.

When it does, the replacement is unlikely to be one of the current disruption-class startup attempts. It is more likely to be a major platform vendor (one of the cloud providers, possibly a major payment-and-settlement vendor, possibly a consortium of the major carriers themselves) that absorbs the inventory-aggregation function into a broader platform with the settlement-and-regulatory infrastructure built in from the start. The replacement, when it comes, will look more like a platform-tier consolidation than a startup-tier disruption.

What the operator class should take from this

For the next ten years, the operator-class read is that the GDS infrastructure persists. Founders building distribution-tech for the airline category should plan to integrate with the GDS as a stable backbone rather than to disrupt it. Carriers running direct-distribution-and-NDC strategies should size the cost of the strategy realistically against the American Airlines benchmark. Investors evaluating GDS-disruption pitches should ask for an answer to all three structural reasons, not just one.

For the longer forecast horizon, the durable read is that the GDS replacement is coming but is unlikely to be the disruption-class startup operating in 2024-2026. The replacement will look like a platform-tier consolidation in the 2030s, with the settlement-and-regulatory infrastructure built in from the start. Operators positioning for that horizon should be building the platform-tier capability or the integration-tier capability that supports it, not the disruption-tier capability that runs against the persistence pattern.

The GDS will outlive every startup that came to disrupt it. American Airlines paid $1.5 billion to prove it again. The next disruption attempt will pay something similar. The pattern persists. The forecast is the forecast. The operator class who read it carefully ship products that work alongside the GDS infrastructure rather than products that promise to replace it. The replacement will come on the longer timeline. The next decade is the GDS decade, again.

—TJ