The OTA take rate is going up. The OTA existential 10-K is the confirmation.

The empirical read on OTA take rates in 2024 is that they are flat-to-up. The major OTA parents have been steadily extracting more from the supply side, with the increases concentrated in the smaller-supply categories that have less negotiating leverage. The data is in the commissioning reports, the hotel-association disclosures, the public 10-K filings of the OTA parents, and the operator-side conversations any hotel chief commercial officer is having quarterly. This is not a contested empirical claim. The take rate is going up.

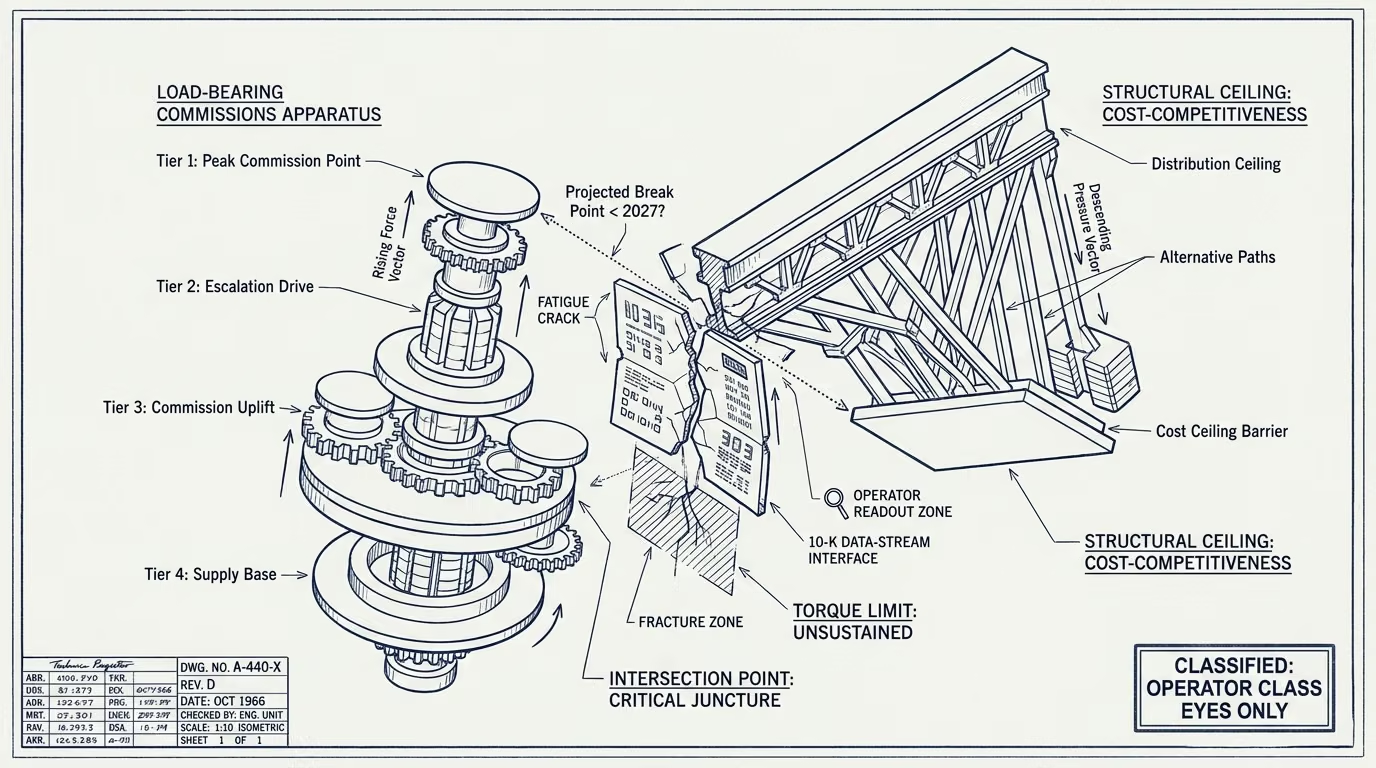

The part that holds is the inverse and is also load-bearing. The OTA parents' 10-K disclosures through 2023-2024 have been adding language about competitive pressure from alternative distribution channels, about supply-side concentration risk, about the long-tail-of-supplier dependency on the OTA channel. The language is increasingly the kind of language that 10-K disclosure conventions require when management thinks the structural picture is shifting in ways the next reporting cycle has to acknowledge. This is the OTA-existential 10-K language. It does not appear when the operator class is confident the take rate is sustainable. It appears when the operator class is hedging against the take rate having to come down.

The two reads cannot both win. The take rate cannot continue going up indefinitely while the structural ceiling keeps rising. One of them breaks before 2027. This essay walks each side, names which side is more likely to break first, and what the part that holds on the timing should be.

The empirical case for take rates going up

The supply-side data through 2022-2024 shows take rates rising on Booking.com, Expedia, and the major regional OTAs by somewhere between half a percentage point and three percentage points, depending on the category and the geography. The increases are not uniform. Large hotel chains with negotiated master agreements have held their rates closer to flat. Independent hotels and smaller regional chains have absorbed the bulk of the increase. Vacation rentals on the OTA platforms have seen meaningful increases. The aggregate take-rate trajectory is up.

The reason this is happening is that the OTA channel is the marginal-customer channel for most of these supply categories, and the supply categories do not have a credible threat to substitute away from the OTA channel. The operator-side leverage in 2024 is structurally weaker than it was in 2018, partly because the consolidation discussed elsewhere has reduced the number of demand-side buyers, partly because the alternative-distribution channels have been slow to mature.

The OTA parents are running the take-rate-increase strategy because the unit economics support it and the supply-side cannot push back at scale. The empirical case is straightforward and the data confirms it.

The structural case for take rates having to come down

The structural case is that the alternative distribution channels have crossed a unit-cost threshold during 2023-2024 that they had not crossed before. Direct-channel customer acquisition for hotels, via paid search, content marketing, loyalty-program-driven direct booking, and the AI-augmented booking tools the chains are deploying, now runs at a unit cost that is competitive with the OTA take-rate equivalent for some categories of customer.

The threshold has been moving for a decade and the trade press has been writing about it for a decade, mostly prematurely. The 2024 version is more credible because the unit-cost data has actually moved. Loyalty-driven direct bookings cost the chain in customer-acquisition dollars somewhere between 8 and 14 percent of the booking value, depending on the chain and the market. The OTA equivalent is 15-25 percent. The gap is not as large as it used to be, the loyalty-direct cost is steady or falling, and the OTA cost is rising. The intersection point is closer than it has been in any prior cycle.

The 10-K disclosure language that has been creeping into the OTA parents' filings reflects management's read on this. The disclosure conventions require that management acknowledge competitive risks that the next reporting cycle should price. The language is not yet aggressive but it has shifted, year over year, in the direction the structural case predicts. The operator class running these companies is hedging, in the disclosure language, against the structural cost-competitiveness threshold the alternative channels are about to cross.

Which side breaks first

The empirical case is what is happening now. The structural case is what has to happen eventually. The interesting question is the timing of when the structural case becomes the dominant read.

The case for the empirical pattern continuing for another two-to-three years is that the OTA channel still has structural leverage in the supply categories where the alternatives have not matured. Vacation rentals at non-Airbnb scale, smaller hotels in regional markets, the long-tail of supply that does not have a meaningful direct-channel option, all continue to depend on the OTA channel and will continue paying the take rate the OTAs charge. The take rates will keep going up in these categories.

The case for the durable read taking over by 2026-2027 is that the cost-competitiveness threshold continues to move in the direction it has been moving, and the AI-augmented direct-channel acquisition that the major hotel chains are deploying compounds in cost effectiveness over the next 24 months. By 2027 the major hotel chains and the larger independents will have direct-channel costs that are below the OTA take rate for the customer cohorts they care most about. The OTA take rates will not be able to rise further on those cohorts without producing the substitution that the disclosure language is hedging against.

The most likely shape of the resolution is a bifurcated outcome. The categories where the alternatives have matured (large hotel chains, large independents in primary markets, large vacation-rental operators) will see take-rate compression starting in 2026 and accelerating through 2027-2028. The categories where the alternatives have not matured (small independents in secondary markets, the long-tail of supply that depends on the OTA channel) will continue to see take rates rise. The OTA aggregate-economics will trend down even as the take rate continues to rise in the categories the OTA parents can still squeeze.

What this leaves the operator class with

The durable read on the OTA take-rate trajectory is more nuanced than either the empirical-only or the structural-only narrative. The take rate is going up where the OTAs can charge it. The take rate has to come down where the alternatives have matured. The two trends will run in parallel through 2025-2026 and the bifurcation will become visible in the OTA parents' financials by late 2026.

For the supply-side operator, the strategic implication is to invest in the direct-channel cost-competitiveness work that the cost-competitiveness threshold is about to validate. The chains that have invested heavily in this through 2023-2024 will be in position to compress their OTA share by 2026-2027. The independents that have not invested will continue paying the rising take rate.

For the OTA parents, the strategic implication is in the disclosure language they are already running. The take-rate-rising era is in its late phase. The take-rate-compressing era is on the horizon. The operator class running these companies is hedging in the 10-K because the operator class running these companies is reading the same thing the careful supply-side observer is reading.

The take rate is going up. The structural ceiling has not moved. The 10-K language is the confirmation that one of the two has to break, and the disclosure conventions are signaling which one. The empirical case has another year or two. The structural case is approaching. Operators positioning for 2027 should be reading the structural case, not the empirical one.

—TJ