TechBio ate the digital health round.

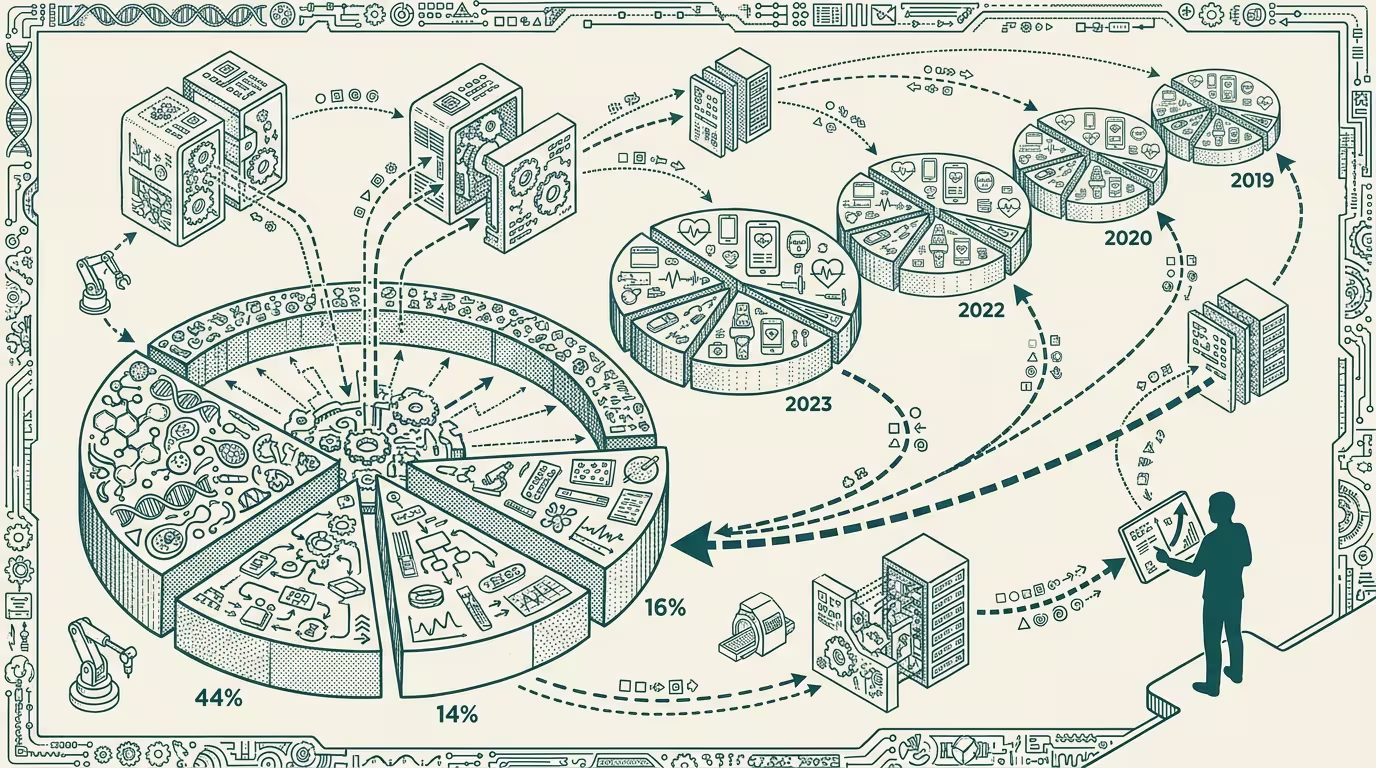

Menlo Ventures' year-end 2024 numbers have a clean read: 58% of US digital-health funding went to AI-enabled ventures, and TechBio captured 44% of that share. Diagnostics took 16%. Operational efficiency took 14%. The remaining slice spread across patient-facing apps, EHR-adjacent SaaS, and the long tail of digital-health-2018 categories that the 2024 capital had mostly stopped funding.

What this inverts is the 2018-2022 narrative. Digital health, for the prior six years, was a consumer-facing category. Patient apps. Telehealth platforms. Wearables-as-services. The investor pitch was that consumer-tech operating models would translate to healthcare. By 2024 most of that pitch had failed: the consumer-acquisition costs were too high, the regulated-category margins were too thin, the health-system buyers wouldn't pay platform-tier prices for what they read as commodity SaaS. The category compressed.

TechBio is the category that ate the round. The pitch is different. Drug discovery accelerated by AI. Biological-mechanism understanding compressed by AI. Computational-biology platforms feeding wet-lab pipelines. The buyer is not the patient or the health system; the buyer is the pharmaceutical industry, and the pharmaceutical industry pays at scale for inputs that improve drug-discovery odds.

The investor-class repositioning is operational. The funds that raised on a "digital health 2018" thesis are, by Q4 2024, repositioning themselves as TechBio-adjacent. Some have hired biology-PhD partners. Some have spun out a TechBio-specific fund. Some have written down the consumer-app portfolio and pretended the new fund's strategy is what they meant all along. The LPs know. The next-fund-raise marketing is, of course, going to claim continuity.

What makes TechBio's economics structurally better than digital health's is that the buyer pays differently. A pharma company evaluating a drug-discovery acceleration tool prices it against the cost of the drug-development pipeline (billions of dollars, decade-long timelines). A health-system evaluating a digital-health tool prices it against IT-budget line items (millions, quarterly review). TechBio captures pricing power from the buyer's frame; digital health gets compressed by it. The category-level margin difference is structural, not cyclical.

What makes the transition harder for founders than for investors is that the digital-health investor class is repositioning faster than the digital-health founder class can. A founder running a 2022-vintage digital-health company in late 2024 does not have a clean path to TechBio. The data is patient-facing, the team is consumer-product-shaped, the GTM is health-system-relationship. None of those map cleanly onto a TechBio company structure. The investor can pivot the fund's thesis on the next raise. The founder cannot pivot the company at the same speed. The mismatch produces a wave of distressed-asset acquisitions in 2025-2026, where the digital-health company sells the data graph to a TechBio buyer and the consumer brand winds down.

What makes the regulatory shape pull the category in the same direction is that the FTC's 2024 health-data rulemaking, the FDA's AI-validation framework, and the broader regulatory frame around AI-in-healthcare all favor the deeper-stack TechBio category over the consumer-facing digital-health category. The TechBio company's regulatory burden is the FDA approval pathway, which is hard but well-understood. The digital-health company's regulatory burden is a patchwork of consumer-protection, HIPAA, state-medical-board, and emerging AI-specific rules that the company has to track across fifty jurisdictions. The category that's easier to regulate against is the category that compounds in the regulated-as-it-tightens environment.

The 2018 digital-health thesis assumed consumer-tech operating models would translate to healthcare. The thesis was wrong. The 2024 TechBio thesis assumes pharma-industry operating models translate to AI-enabled biology. The thesis is, on the available evidence, less wrong, but it also has not been tested at the scale the capital is now pricing. Some of the TechBio capital deployed in 2024 will look, in 2027, like the digital-health capital deployed in 2018: convinced of a structural shift that turned out to be smaller than the deck implied.

Cut through the venture-press read and the picture sharpens. TechBio ate the digital-health round because the digital-health round had run out of things worth buying, and the capital had to land somewhere. TechBio is, on structural grounds, a better category. It is not, on the absolute scale of the capital flowing into it, a category large enough to absorb the deployment without producing some fraction of overpriced bets.

The operators who recognize this in 2024 are the operators who allocate against the strongest TechBio companies on conservative multiples. The operators who treat the entire TechBio category as the next Magnificent Seven are the operators paying the vintage-2024 premium for what's going to look like vintage-2018 digital-health in 2027. Both will be true. The category compounds. The vintage gets repriced.

—TJ