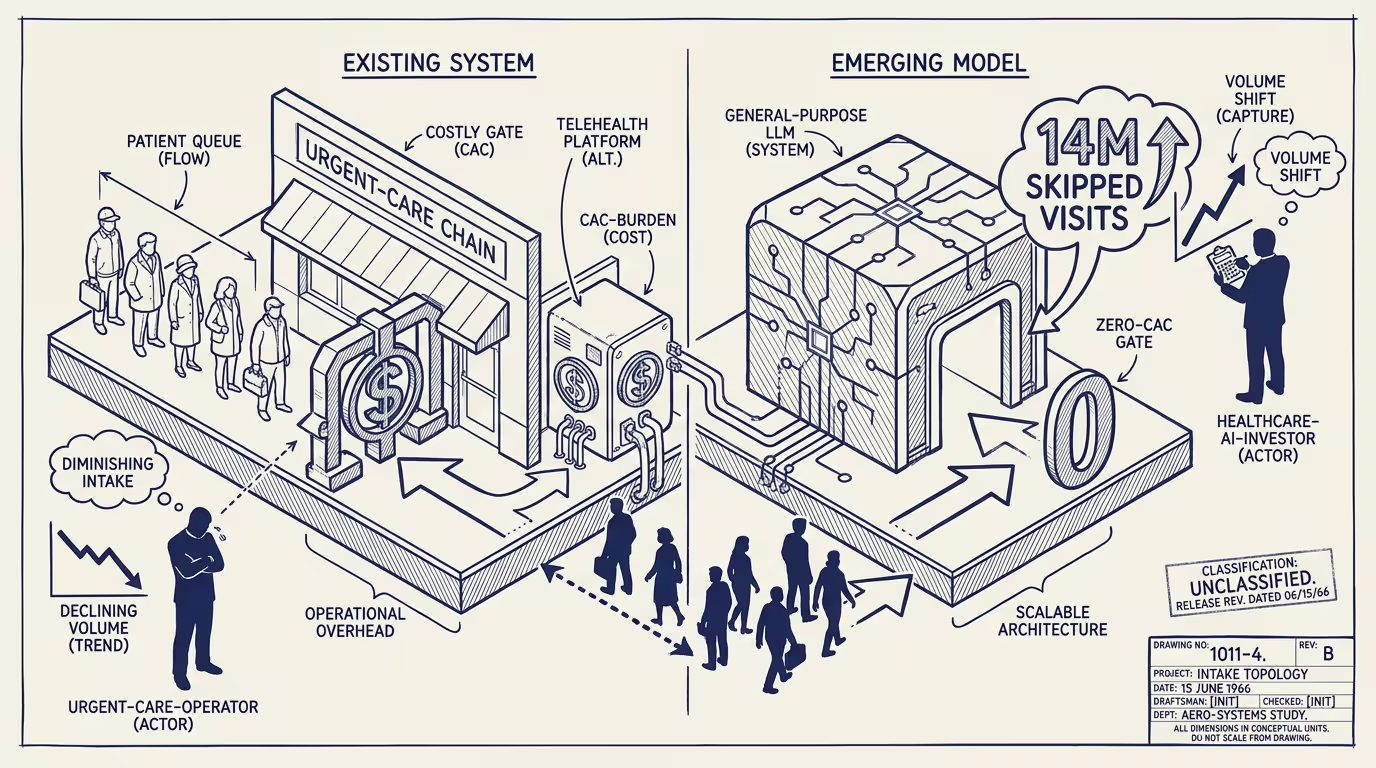

Urgent care has a competitor with no CAC.

Gallup/West Health published joint research in early Q2 2026 on consumer AI usage for health information. 25% of Americans had used an AI tool for health information in the past 30 days. 14 million adults reported skipping a provider visit they would have otherwise made because they got the answer from an AI. The cited reasons split: 14% cost, 16% access.

The trade press read the data as another consumer-AI adoption metric. The healthcare-AI investor class read it as evidence of category expansion.

_Urgent care has a competitor with no CAC._ The competitor isn't another urgent-care chain or another telehealth platform. The competitor is the general-purpose LLM that the consumer already has installed, with no acquisition cost and no marginal cost per query.

Look at the unit economics side by side. Urgent care chains operate at roughly $150-300 customer-acquisition cost per new patient and $50-150 per-visit margin. Telehealth platforms operate at roughly $80-200 CAC and $20-80 per-visit margin. General-purpose LLMs operate at $0 CAC for the consumer (they're already paying for ChatGPT, Claude, or Gemini for non-health uses) and effectively zero per-query cost from the consumer's perspective. When the consumer's question is low-acuity (mild symptoms, medication interactions, basic health information), the LLM produces an answer that the consumer accepts as sufficient. The visit doesn't happen. The urgent-care or telehealth provider loses the volume that the LLM substituted for.

What does the substitution actually displace? Not premium clinical care. AI is displacing the bottom of the digital-health funnel. The consumer who skips an urgent-care visit because the LLM answered their question is the consumer at the low-acuity / low-margin end of the urgent-care spectrum. Premium clinical care (specialist consultation, complex diagnostic work, procedure-class care) is structurally protected because the LLM doesn't substitute for it. Low-acuity / high-volume care is structurally exposed because that's exactly where the LLM substitutes well. The market-structure inflection is asymmetric: premium care continues to grow; low-acuity volume compresses. Urgent care chains and basic-telehealth platforms are positioned in the compression zone.

The operator-class response is to either move up the acuity curve or build an LLM-mediated front-door of their own. Move-up: reposition urgent-care and telehealth platforms toward higher-acuity care where LLMs don't substitute. Requires investment in clinical-staff capability, regulatory positioning for higher-acuity categories, and brand repositioning that moves away from the convenience framing. Build LLM-front-door: add an AI-mediated triage layer that serves the low-acuity questions for free, captures the consumer's healthcare relationship, and routes the higher-acuity cases to the chain's clinical infrastructure. Both strategies are operating-coherent. Continuing to compete on legacy positioning against the no-CAC competitor is operationally unsustainable.

What's the regulatory frame doing? Operating-permissively. Consumer-protection regulation for healthcare-AI focuses on FDA-class approval for AI-enabled diagnostic devices and HIPAA-class compliance for AI-enabled clinical software. General-purpose consumer LLMs answering health questions sit outside both frameworks. The FDA hasn't moved to regulate consumer-LLM health information; HIPAA doesn't apply to consumer-class LLM interactions. Through 2026-2028 the substitution proceeds under regulatory ambiguity. Urgent-care and telehealth platforms cannot rely on regulatory friction to slow the LLM substitution. The substitution will continue at the rate consumer trust in LLM health information builds.

The same shape recurs across categories where general-purpose LLMs substitute for the low-end of category-specific demand. Legal services: low-complexity questions answered by LLMs displace the bottom of consumer-legal-service volume. Tax preparation: simple-return preparation by LLMs displaces the bottom of consumer-tax-prep volume. Financial advisory: basic financial questions answered by LLMs displace the bottom of robo-advisor volume. Each category has the same structural shape: premium professional services protected, low-end volume compressed, market-structure inflection driven by the LLM's zero-CAC competitive advantage.

What survives all of this is that the Gallup/West Health 2026 data is one of the cleaner public quantifications of consumer-LLM substitution for low-acuity healthcare visits, the substitution is structurally durable through the next 24-36 months at minimum, and the operator-grade strategy for urgent-care and telehealth chains is to either move up the acuity curve or build their own LLM-front-door. Operators executing either strategy are operating-coherent. Operators continuing to compete on legacy positioning are absorbing the substitution as a market-wide volume compression they cannot reverse.

Urgent care has a competitor with no CAC. The competitor is structurally protected from the regulatory frame that would otherwise constrain it. The market-structure inflection is asymmetric and the bottom-of-funnel volume is compressing in real time. By 2028 the cohort-level data on urgent-care visit volumes will show the compression clearly. The operator who repositioned in 2026 is the cohort whose 2028 metrics survive the inflection.

—TJ